ETFs — exchange-traded funds — are one of the most powerful and misunderstood tools in personal investing. They're the reason ordinary investors can now hold tiny pieces of hundreds of companies for near-zero cost, trade them like a stock, and build a diversified portfolio in a single purchase. If you've heard of index funds but aren't sure how ETFs fit in, this guide clears it up completely.

What Is an ETF?

An ETF is a fund that holds a basket of assets (stocks, bonds, commodities) and trades on a stock exchange throughout the day, just like shares of Apple or Tesla. When you buy one share of VTI (Vanguard Total Stock Market ETF), you're buying fractional ownership of approximately 3,700 US companies in a single transaction.

The key difference from mutual funds: ETFs trade in real time during market hours. Mutual funds are priced once per day at market close. For long-term investors, this distinction rarely matters — but ETFs are often slightly more tax-efficient in taxable accounts.

ETF vs Mutual Fund vs Individual Stock

| Feature | ETF | Mutual Fund | Individual Stock |

|---|---|---|---|

| Diversification | High (holds many assets) | High (holds many assets) | None (single company) |

| Trading | Real-time (stock exchange) | Once daily (end of day) | Real-time |

| Typical cost | 0.03–0.20% (index ETFs) | 0.05–1.50% (varies widely) | $0 commission |

| Minimum investment | Price of one share (often $50–$400) | Often $0–$1,000 | $1 (fractional shares) |

| Tax efficiency | High | Moderate | High |

| Best for | Diversified long-term investing | Retirement accounts, automation | Individual company conviction |

Types of ETFs: What You Need to Know

Not all ETFs are created equal. The category matters:

Index ETFs (What Most Beginners Should Use)

These track a specific index like the S&P 500, total US market, or total bond market. They're passively managed — no fund manager is making decisions, the fund just replicates the index. This means:

- Very low fees (0.03–0.07% typically)

- Predictable, transparent holdings

- Historically outperforms most actively managed funds over long periods

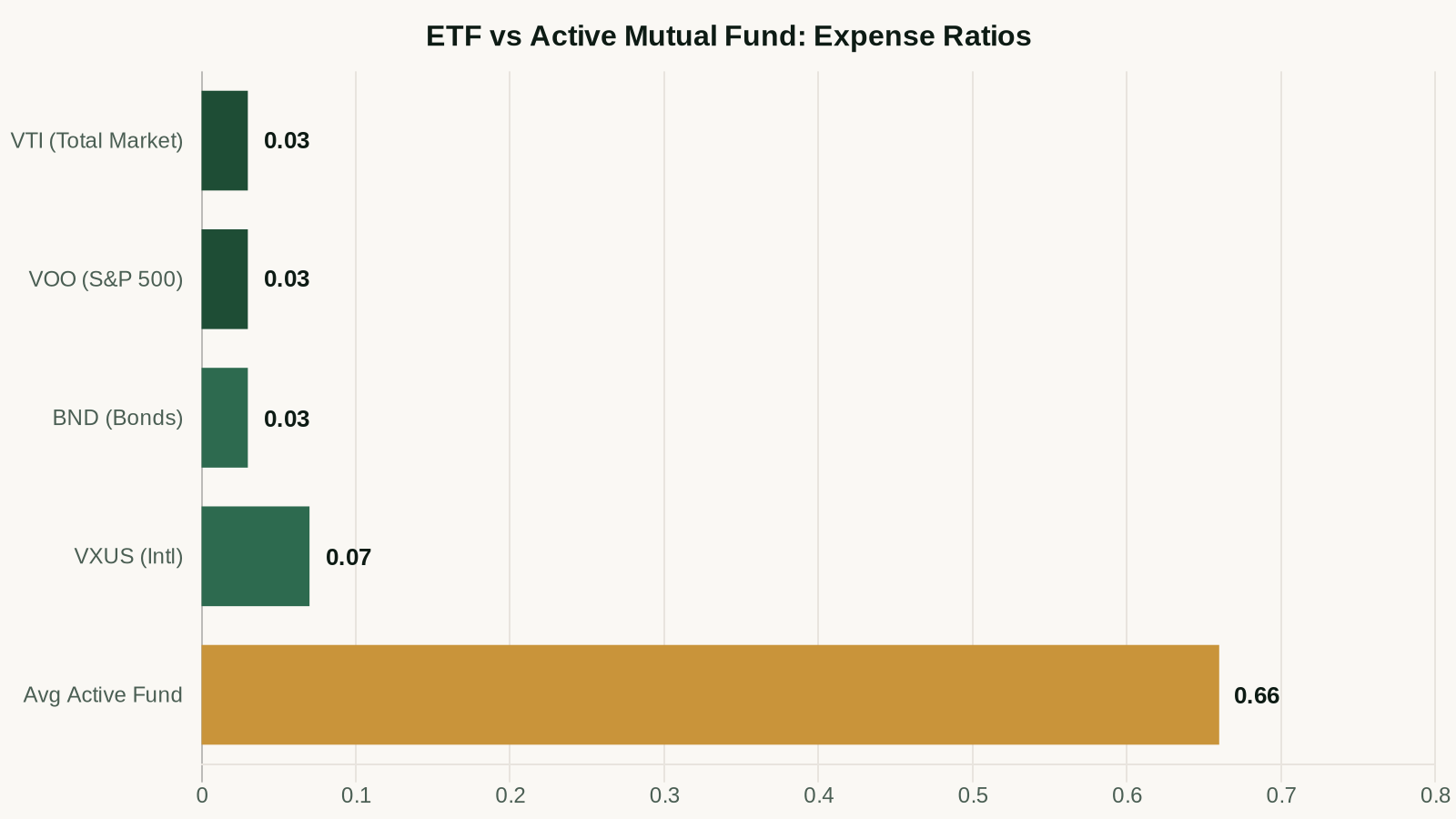

Examples: VTI (total US), VOO (S&P 500), VXUS (international), BND (bonds)

Sector ETFs

Concentrate in a specific industry: technology (QQQ), healthcare, energy, financials. Higher potential returns in boom sectors, but much higher volatility. Not recommended as core holdings for beginners — reserve for less than 10% of your portfolio if at all.

Bond ETFs

Hold a basket of bonds. Lower return potential than stock ETFs, but lower volatility. BND (Vanguard Total Bond) and AGG (iShares Core US Aggregate Bond) are the standards. Appropriate as the "steady" portion of a portfolio, particularly for investors closer to retirement.

Leveraged and Inverse ETFs

Designed to amplify or reverse market returns. AVOID as a beginner. They decay in value over time due to daily rebalancing mechanics and are designed for day traders, not investors.

The Best ETFs for Beginners in 2026

For a beginner building a long-term portfolio, you need at most three ETFs:

- VTI — Vanguard Total Stock Market ETF, 0.03% expense ratio. Holds ~3,700 US companies. This alone covers all of your domestic equity exposure.

- VXUS — Vanguard Total International Stock ETF, 0.07% expense ratio. Adds developed and emerging market exposure. Target 20–30% of equity allocation.

- BND — Vanguard Total Bond Market ETF, 0.03% expense ratio. Reduces volatility. Under 40, keep this at 10% or less.

That's it. Three ETFs. Total annual cost on $10,000: about $5. This portfolio has historically captured market returns with maximum diversification at minimum cost.

How to Buy Your First ETF: Step by Step

- Open a brokerage account: Fidelity, Webull, or Vanguard. All offer commission-free ETF trading.

- Deposit funds: Transfer from your checking account. ETFs require purchasing at least one full share (or use fractional shares if your broker supports it).

- Search the ETF ticker: e.g., "VTI"

- Place a market or limit order: Market order buys at the current price immediately. Limit order lets you set a maximum price. For long-term investors, market orders are fine.

- Enable dividend reinvestment (DRIP): Most brokers allow this in account settings. Your dividends automatically buy more shares, accelerating compounding.

- Set a recurring purchase schedule: Monthly contributions on the same day each month. Dollar-cost averaging removes the anxiety of timing the market.

Open a Fidelity Account for Commission-Free ETFs →

ETF Tax Considerations

In a tax-advantaged account (Roth IRA, 401k), taxes on ETF gains are deferred or eliminated entirely. In a taxable brokerage account:

- Long-term capital gains (held 1+ year): Taxed at 0%, 15%, or 20% depending on your income. Most investors pay 15%.

- Short-term capital gains (held less than 1 year): Taxed as ordinary income — can be 22–37%.

- Dividends: Qualified dividends are taxed at the same low rate as long-term capital gains. Ordinary dividends at your income tax rate.

Strategy: Hold your highest-growth ETFs in tax-advantaged accounts (Roth IRA), and if you need to hold ETFs in a taxable account, prefer broad market ETFs that are tax-efficient by nature.

Common Beginner ETF Mistakes

- Buying too many ETFs: 10–15 ETFs with overlapping holdings isn't diversification — it's confusion. Three well-chosen ETFs do the job better.

- Chasing recent performance: Sector ETFs that topped last year's rankings typically mean-revert. Stick to broad index ETFs.

- Checking balance too frequently: Daily checking leads to panic selling during downturns. Set contributions to automatic and review quarterly.

- Confusing leveraged ETFs with regular ETFs: The ticker "SPXL" (3x S&P 500) and "VOO" (1x S&P 500) look similar but behave completely differently. Always check the fund description before buying.

Frequently Asked Questions

Can ETFs lose value?

Yes. ETFs that hold stocks go up and down with the market. A total market ETF like VTI dropped roughly 33% in early 2020 and 20% in 2022 before recovering. Long-term investors who stayed invested recovered fully and then some. Short-term, yes — ETFs carry market risk.

Do ETFs pay dividends?

Most stock ETFs pay dividends quarterly. VTI's dividend yield is approximately 1.4–1.8%. These are distributed to shareholders and can be automatically reinvested. Bond ETFs like BND pay dividends monthly.

What's the minimum amount to invest in an ETF?

The minimum is one share, which varies by ETF price. VTI trades around $240/share. With fractional shares at Fidelity, Webull, and Robinhood, you can invest as little as $1. Starting with $100 is entirely feasible with fractional share support.

Is there a difference between Vanguard ETFs and Fidelity index funds?

Functionally very similar. Vanguard ETFs (VTI, VXUS, BND) can be held at any brokerage. Fidelity's zero-cost mutual funds (FZROX, FZILX) can only be held at Fidelity but have 0% expense ratios vs. 0.03–0.07% for Vanguard ETFs. For Fidelity account holders, the Fidelity zero funds are marginally better. For everyone else, Vanguard ETFs are the standard choice.

10 Income Streams Blueprint

Build 10 distinct income streams with AI doing the heavy lifting. 42-page system, 30-day plan, done-for-you tracker.

$97 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.