Over any 20-year period, more than 90% of actively managed mutual funds have underperformed their benchmark index — while charging you 0.5–1.5% in annual fees to do it. Index funds solve this in the simplest possible way: instead of paying a manager to try and beat the market, you just buy the market. Here are the best index funds for beginners in 2026.

Best Index Funds for Beginners: Quick Comparison

| Fund | What It Tracks | Expense Ratio | Available At | Best For |

|---|---|---|---|---|

| FZROX ⭐ Best Overall | Total US Stock Market | 0.00% | Fidelity only | Roth IRA / 401k at Fidelity |

| VTI (Vanguard) | Total US Stock Market | 0.03% | Any brokerage | Taxable accounts, portability |

| FZILX | Total International Market | 0.00% | Fidelity only | International diversification |

| VXUS (Vanguard) | Total International Market | 0.07% | Any brokerage | International allocation, portable |

| FXNAX / BND | US Bond Market | 0.025% / 0.03% | Fidelity / Any | Bond allocation, risk reduction |

| VOO / FXAIX | S&P 500 | 0.03% / 0.015% | Any / Fidelity | Large-cap US equities |

Why Expense Ratios Matter More Than You Think

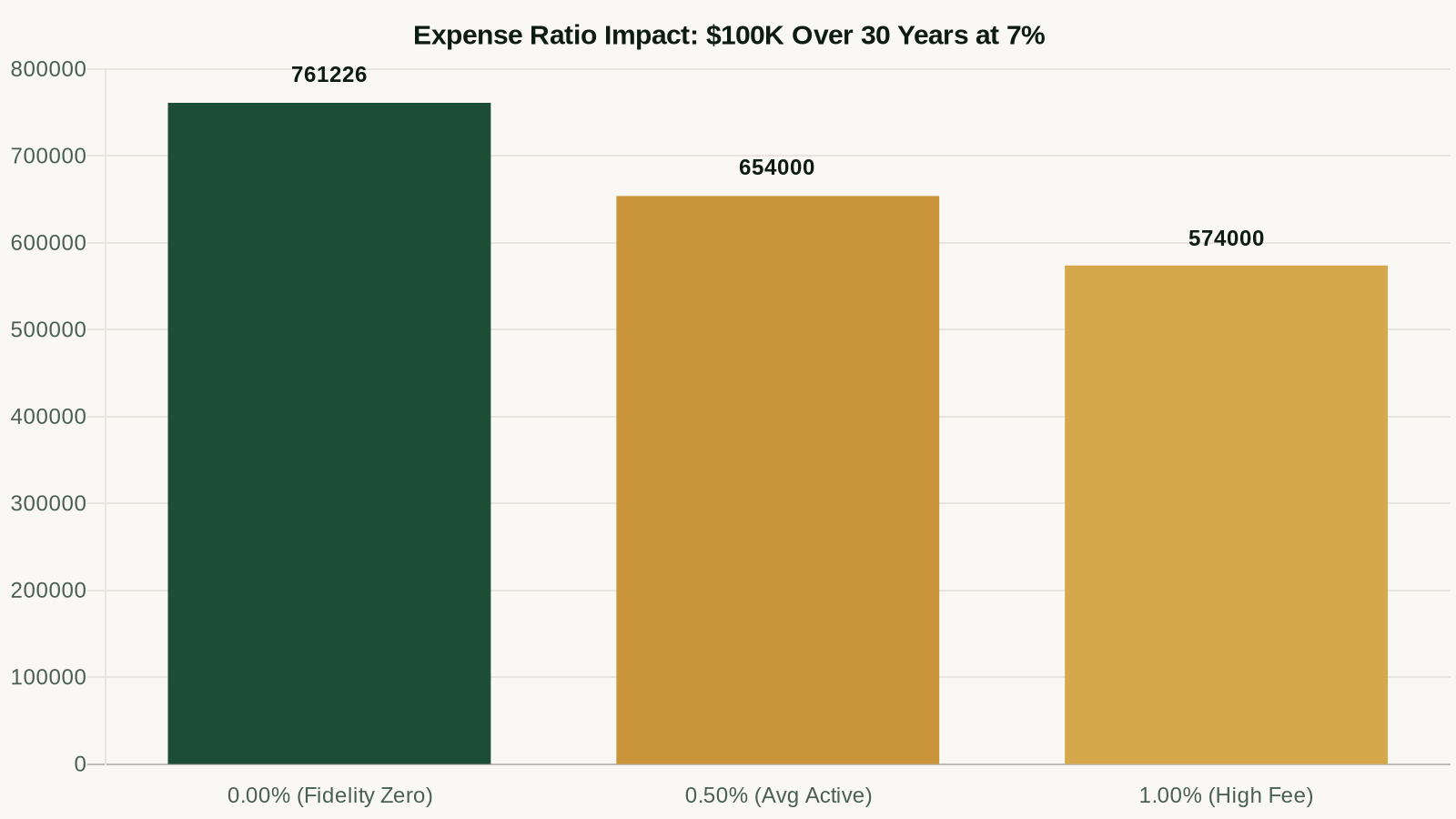

An expense ratio is the annual fee a fund charges, expressed as a percentage of your invested assets. It's deducted automatically — you never write a check. But the compounding effect is significant:

- $100,000 invested for 30 years at 7% average return:

- 0.00% expense ratio: $761,226

- 0.50% expense ratio: $654,000 (cost: $107,000)

- 1.00% expense ratio: $574,000 (cost: $187,000)

A 1% expense ratio doesn't sound like much. Over 30 years, it costs you $187,000 on a $100,000 investment. The zero-cost funds available at Fidelity eliminate this entirely.

The Three-Fund Portfolio: The Simplest Strategy That Works

Most financial experts agree that a three-fund portfolio covering US stocks, international stocks, and bonds is all most investors need. It provides diversification across thousands of companies and asset classes with no overlap.

Classic Three-Fund Setup at Fidelity (Zero Cost)

- FZROX (~70%): Total US stock market — thousands of US companies in one fund

- FZILX (~20%): Total international stock market — developed and emerging market exposure

- FXNAX (~10%): US bond index — reduces portfolio volatility

Total annual cost: $0. This is genuinely free. No fund company in the world offers a lower cost than 0%.

Classic Three-Fund Setup at Vanguard (Nearly Zero Cost)

- VTI (~70%): Total US stock market, 0.03% expense ratio

- VXUS (~20%): Total international stock market, 0.07% expense ratio

- BND (~10%): US bond market, 0.03% expense ratio

Total annual cost on $10,000: about $5/year. Effectively free.

Open a Fidelity Account to Access FZROX →

S&P 500 vs. Total Market Index: Which Is Better?

This is a common question. The S&P 500 (tracked by VOO, FXAIX, SPY) holds 500 large US companies. A total market fund (VTI, FZROX) holds 3,000–4,000 companies including small- and mid-cap stocks.

The practical difference is small — the S&P 500 represents about 80% of the total US stock market by weight. But over long periods, small-cap stocks have historically outperformed large-caps slightly. The total market fund captures that premium with no additional cost. For a beginner, either is excellent; the total market fund is marginally better in theory.

How to Allocate Your Portfolio

For Investors Under 40

The classic 90/10 or 80/20 (stocks/bonds) portfolio works well. With 30+ years until retirement, you have time to ride out market downturns. Consider:

- 70% FZROX (or VTI)

- 20% FZILX (or VXUS)

- 10% FXNAX (or BND)

For Investors 40–55

Start shifting toward more bonds as retirement approaches:

- 60% US stocks

- 20% International stocks

- 20% Bonds

The Lazy Alternative: Target-Date Funds

If you don't want to think about allocation at all, a target-date fund automatically adjusts from stock-heavy to bond-heavy as you approach your target retirement year. Fidelity's Freedom Index funds are low-cost (0.12%) and do the work for you. Slightly less optimized than the three-fund portfolio, but still excellent and completely hands-off.

Where to Open Your Index Fund Account

Fidelity is the best choice for most beginners — zero-expense-ratio funds, no minimums, fractional shares, and excellent customer service. After Fidelity, Vanguard (the originator of index investing) and Charles Schwab are both solid options.

- Fidelity — Best overall, zero-cost proprietary funds

- Vanguard — Best for portability (ETF versions can be held anywhere)

- Schwab — Good option, competitive funds, strong banking integration

Avoid opening index fund accounts at traditional banks — their fund options are limited and often more expensive.

Frequently Asked Questions

Are index funds safe?

Index funds are subject to market risk — they will go down during market downturns. But because they hold thousands of companies, they can't go to zero (which individual stocks can). Over any 20-year period in history, the US stock market has been higher at the end than at the beginning. Long-term investors historically have been rewarded for staying invested through downturns.

How often should I rebalance my portfolio?

Once a year is sufficient for most investors. Rebalancing means selling funds that have grown above your target allocation and buying ones below. At Fidelity, you can set automatic rebalancing. If you're using a target-date fund, it rebalances automatically.

Should I invest a lump sum or dollar-cost average?

Research shows lump-sum investing outperforms dollar-cost averaging about two-thirds of the time (because markets trend upward, so investing earlier captures more of the gain). But if a lump sum would cause you anxiety and make you sell during a dip, dollar-cost averaging is better psychologically — and better than not investing at all.

What's the difference between a mutual fund and an ETF version of the same index?

For most practical purposes, they're identical. ETFs trade during the day like stocks; mutual fund versions are priced once per day at market close. ETFs have slightly more tax efficiency in taxable accounts. For retirement accounts (Roth IRA, 401k), the difference is negligible — pick whichever minimum suits you (ETFs can require a full share purchase at some brokers, while mutual funds allow any dollar amount).

10 Income Streams Blueprint

Build 10 distinct income streams with AI doing the heavy lifting. 42-page system, 30-day plan, done-for-you tracker.

$97 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.