A Roth IRA is one of the best wealth-building tools available to ordinary people. Tax-free growth for decades. No required minimum distributions. The ability to withdraw contributions penalty-free any time. And most people either don't have one or haven't contributed to it this year.

Here's everything you need to know to decide if a Roth IRA is right for you — and how to open one today.

Free Resource

Ready to put the Roth IRA to work?

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →What Is a Roth IRA?

A Roth IRA is an individual retirement account funded with after-tax money. The tradeoff for contributing money you've already paid taxes on: your money grows completely tax-free, and withdrawals in retirement are also tax-free.

Compare this to a traditional IRA or 401(k), which gives you a tax deduction upfront but taxes you when you withdraw in retirement. The Roth is better if you expect to be in a higher tax bracket in retirement than you are today — which is true for most people in their 20s and 30s.

2026 Roth IRA Contribution Limits

| Age | 2026 Contribution Limit | Income Limit (Single) | Income Limit (Married) |

|---|---|---|---|

| Under 50 | $7,000 | Phase out $150k–$165k | Phase out $236k–$246k |

| 50 and older | $8,000 (catch-up) | Same | Same |

Note: If your income exceeds the phase-out range, you can't contribute directly to a Roth IRA. However, you may be able to use the "backdoor Roth" strategy — consult a tax advisor if you're near these limits.

Roth IRA vs. Traditional IRA: Which Is Better?

The answer depends on when you think your tax rate will be higher: now or in retirement.

- Choose Roth if: you're early in your career, expect income to grow significantly, or want maximum withdrawal flexibility

- Choose Traditional if: you're in a high tax bracket now and expect to drop significantly in retirement

- Do both if: you have the cash flow — max your employer 401(k) match first, then contribute to a Roth IRA

For most people in their 20s and 30s, the Roth IRA wins. You're likely in a lower tax bracket now than you'll be at 65, and you're locking in decades of tax-free compound growth.

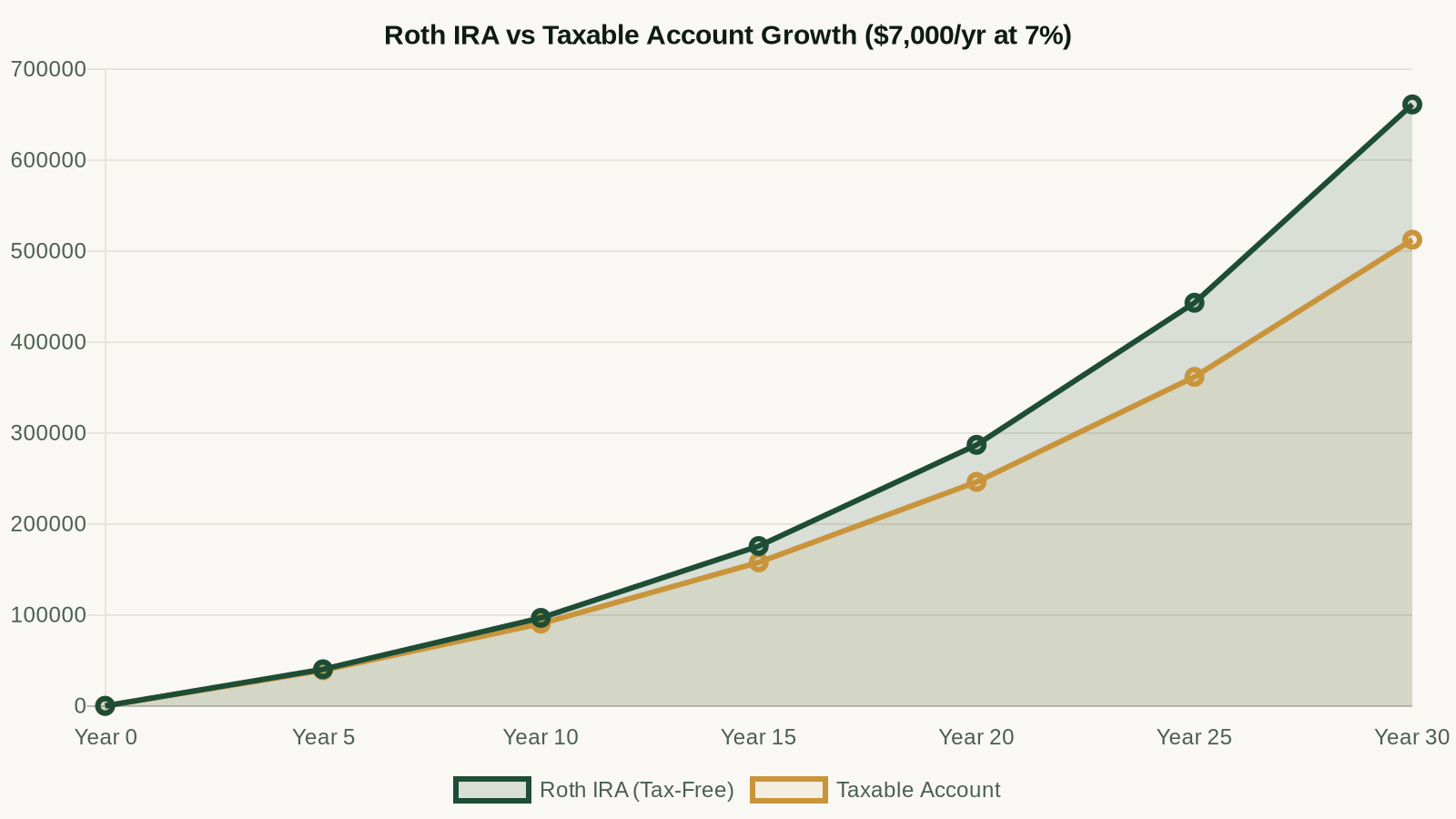

The Power of Starting Early

Here's the math on what $7,000/year in a Roth IRA looks like over time, assuming a 7% average annual return:

- Starting at 25: ~$1.9M by 65

- Starting at 35: ~$950K by 65

- Starting at 45: ~$440K by 65

Waiting 10 years doesn't cost you 10 years of contributions — it cuts your ending balance roughly in half. The best time to open a Roth IRA is today.

Best Places to Open a Roth IRA in 2026

1. Fidelity — Best Overall

Fidelity has the best combination of features for most investors: zero-expense-ratio index funds, fractional shares, excellent research tools, and no account minimums or fees. Their mobile app is strong, and their customer support is available 24/7.

Best for: Long-term index fund investors who want the best platform at zero cost.

2. Betterment — Best for Hands-Off Investors

If you want a Roth IRA that manages itself, Betterment's 0.25% annual fee gets you automated portfolio management, tax-loss harvesting within the taxable account, and automatic rebalancing. You pick a risk level, connect your bank, and it handles everything else.

Best for: People who want to invest consistently without managing their portfolio.

3. Webull — Best for Active Traders

If you want to actively pick stocks inside your Roth IRA, Webull offers commission-free trading with strong charting tools. Not the default choice for most people, but solid if you're going the self-directed route.

Best for: Active investors who pick individual stocks.

What to Invest In Inside Your Roth IRA

The account structure is just the container. What you put in it matters. For most people, a simple three-fund portfolio works well:

- Total US Stock Market Index Fund (~70%) — broad exposure to US equities

- Total International Stock Market Index Fund (~20%) — international diversification

- US Bond Index Fund (~10%) — reduces volatility as you approach retirement

At Fidelity, this is FZROX + FZILX + FXNAX — all with zero expense ratios. The simplest, lowest-cost approach to retirement investing that has consistently beaten most actively managed funds over 20-year periods.

How to Open a Roth IRA: Step by Step

- Choose a provider (Fidelity is our recommendation)

- Click "Open an Account" → select "Roth IRA"

- Enter personal information (SSN, address, employment status)

- Fund the account — you can contribute up to $7,000 for 2026, but start with whatever you have

- Select your investments (or let it sit in a money market fund temporarily)

- Set up automatic monthly contributions so it grows on autopilot

Total time: 15–20 minutes. The hardest part is starting. Once it's open, set a recurring transfer and let compound interest do the work.

Related: Once your Roth IRA is set up, make sure your cash savings are also earning the highest rate available. See our HYSA rankings →

10 Income Streams Blueprint

Build 10 distinct income streams with AI doing the heavy lifting. 42-page system, 30-day plan, done-for-you tracker.

$97 one-time

Keep Reading

Recommended Product

Want to learn how to build 10 income streams?

The 10 Income Streams Blueprint ($97) walks you through the complete framework for building multiple income sources — from side hustles to scalable businesses.

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.