The average savings account at a traditional bank pays 0.46% APY. The best high-yield savings accounts available right now pay more than 10x that. If you have $20,000 in an old savings account, you're leaving $930/year on the table.

We evaluated 12 HYSAs on APY, fees, minimum deposits, mobile experience, and FDIC coverage. Here's what we found.

Free Resource

Want a step-by-step guide to start investing today?

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →Our Top Picks at a Glance

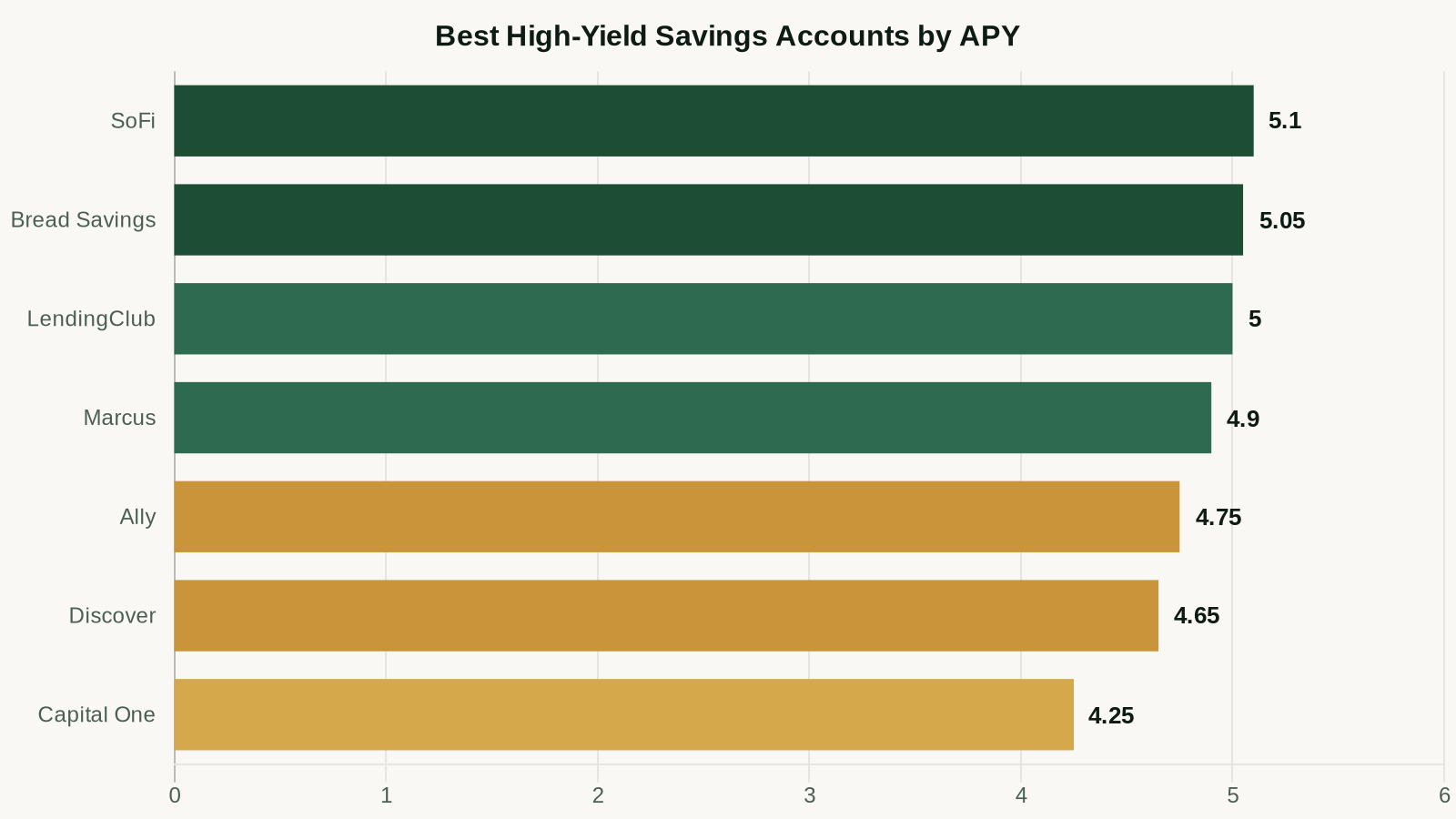

| Account | APY | Min. Deposit | Monthly Fee | FDIC? |

|---|---|---|---|---|

| SoFi Savings ⭐ Best Overall | 5.10% | $0 | $0 | Yes |

| Marcus by Goldman Sachs | 4.90% | $0 | $0 | Yes |

| Ally Bank | 4.75% | $0 | $0 | Yes |

| Traditional Big Bank (avg) | 0.46% | Varies | Often $5–$15 | Yes |

Why Your Current Savings Account Is Costing You Money

Let's do the math. At 0.46% APY, $50,000 earns $230/year. At 5.10% APY, the same $50,000 earns $2,550/year. That's a $2,320 annual difference — and all you have to do is move the money.

The five pain points we hear from readers about their current savings accounts:

- Invisible fees — maintenance charges that eat into already-low interest

- Outdated APYs — rates that haven't kept pace with Federal Reserve increases

- Clunky mobile apps — making it hard to manage and move money

- Low or no FDIC coverage — some fintech "savings" accounts aren't bank accounts at all

- Hidden restrictions — transfer limits, rate tiers, or balance minimums buried in fine print

Best High-Yield Savings Accounts: Detailed Reviews

1. SoFi High-Yield Savings — Best Overall

APY: 5.10% | Minimum: $0 | Monthly Fee: $0

SoFi's savings account leads the pack on rate and combines it with a genuinely good mobile experience. You get direct deposit integration, automated saving features, and FDIC coverage up to $2M through a network of partner banks.

The 5.10% rate applies when you have direct deposit set up or deposit $5,000+ per month. Without direct deposit, the rate is still competitive at 4.60%. For most people with a day job, you'll hit the higher tier automatically.

Best for: People who want the highest APY with no hoops to jump through.

2. Marcus by Goldman Sachs — Best for Simple Savers

APY: 4.90% | Minimum: $0 | Monthly Fee: $0

Marcus has been a consistent high-yield option since launching in 2016. No minimums, no fees, and a clean interface. They don't offer checking accounts, which keeps the experience focused. The Goldman Sachs backing also provides a layer of institutional credibility you don't get with newer fintechs.

Best for: People who want a well-established institution with a clean, no-frills product.

3. Ally Bank — Best Full-Service Online Bank

APY: 4.75% | Minimum: $0 | Monthly Fee: $0

Ally is the best option if you want to consolidate your banking entirely. You get a competitive HYSA, a checking account, CDs, investment accounts, and an excellent mobile app — all under one roof. The slightly lower APY is the tradeoff for the ecosystem.

Best for: People who want to replace their traditional bank entirely.

How to Open a High-Yield Savings Account (Takes 10 Minutes)

- Pick an account from the list above (we recommend SoFi as the default)

- Go to the bank's website and click "Open Account"

- Enter your Social Security number, address, and date of birth

- Fund the account with an initial transfer from your current bank (usually $1–$100 to start)

- Set up recurring transfers from your checking account

The whole process takes about 10 minutes. Your new account will be fully active within 1–3 business days.

HYSA vs. Money Market Accounts: What's the Difference?

Both are FDIC-insured, both offer higher rates than traditional savings, and both are low-risk places to hold cash. The main differences:

- HYSAs: Usually online-only, slightly higher rates, simpler product

- Money Market Accounts (MMAs): Sometimes include check-writing privileges, may require higher minimums

For most people building an emergency fund or parking short-term savings, a HYSA is the simpler and usually better-paying choice.

How Much Should Be in Your HYSA?

Use your HYSA for:

- Emergency fund: 3–6 months of expenses (this is the primary use case)

- Short-term savings goals: Vacation, down payment, car — anything you need within 3 years

- Waiting room money: Cash you're about to invest but haven't deployed yet

Don't over-stuff your HYSA. Cash earning 5% is still losing to inflation over the long run. Money you won't need for 5+ years belongs in the market.

Next step: After you've set up your HYSA, the next move is making sure your investment accounts are also optimized. Read our Roth IRA guide →

Budget Blueprint Kit

Zero-to-surplus budgeting done in an afternoon. PDF guide, auto-calculating Excel tracker, and AI prompt library included.

$27 one-time

Keep Reading

Recommended Product

Want to learn how to build 10 income streams?

The 10 Income Streams Blueprint ($97) walks you through the complete framework for building multiple income sources — from side hustles to scalable businesses.

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.