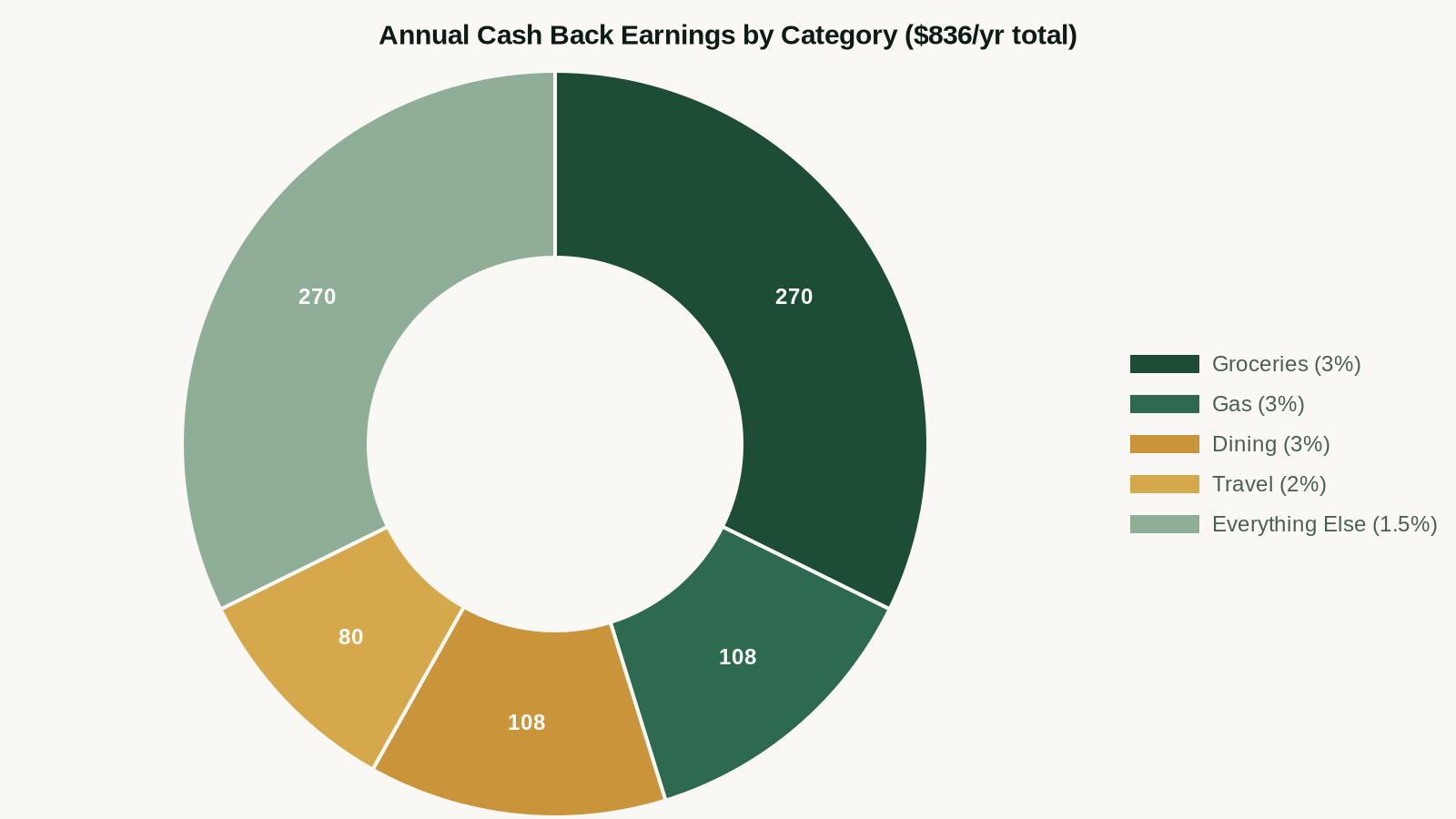

A well-chosen cash back credit card earns you $600–$1,200/year on spending you're already doing. That's a meaningful return with zero investment risk — as long as you pay the balance in full each month (which is non-negotiable).

We analyzed 8 top cash back cards by rewards rate, annual fee, sign-up bonus, and redemption flexibility. Here are the results.

Free Resource

Building wealth takes more than cash back cards.

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →Best Cash Back Cards at a Glance

| Card | Base Rate | Best Category | Annual Fee | Sign-Up Bonus |

|---|---|---|---|---|

| Chase Freedom Unlimited ⭐ Best No-Fee | 1.5% | 3% dining/drugstores | $0 | $200 after $500 spend |

| Citi Double Cash | 2% (1% + 1%) | Flat rate everything | $0 | $200 after $1,500 spend |

| Amex Blue Cash Preferred | 1% | 6% US supermarkets | $95 | $250 after $3,000 spend |

| Discover it Cash Back | 1% | 5% rotating categories | $0 | Match first-year cash back |

The Five Mistakes People Make With Credit Cards

- Carrying a balance — This immediately eliminates your rewards. At 20%+ APR, the math never works. Cash back cards only make sense if you pay in full.

- Using the wrong card for the category — Grocery shopping with a flat 1.5% card instead of a 6% grocery card costs you real money over a year

- Ignoring sign-up bonuses — A $200 sign-up bonus after $500 spend is a guaranteed 40% return on your first $500. Don't leave it behind.

- Too many cards — The complexity of managing 6+ cards usually results in missed payments and hurt credit scores. Two or three well-chosen cards is the sweet spot.

- Annual fees without justification — Only pay an annual fee if the rewards you earn exceed it by a margin that justifies the complexity.

Best Cash Back Cards: Detailed Reviews

1. Chase Freedom Unlimited — Best Overall No-Fee Card

1.5% base | 3% dining & drugstores | No annual fee

The Freedom Unlimited is our default recommendation for most people. You earn 1.5% on everything, 3% on dining, and 3% at drugstores — with zero annual fee and a solid $200 sign-up bonus. If you have a Chase Sapphire card, your cash back can be converted to transferable points, significantly increasing the value.

The card is also a good first card for people building credit — Chase's application standards are reasonable, and the rewards are immediate.

Apply for Chase Freedom Unlimited →

2. Citi Double Cash — Best Flat-Rate Card

2% on everything (1% when you buy + 1% when you pay) | No annual fee

If you want the simplicity of one card that earns well on everything, the Citi Double Cash is hard to beat. No categories to track, no rotating rewards, no activation required. Just 2% back on every dollar — which beats most "category" cards on non-bonus spend.

Best for: People who want one simple card for all purchases.

3. Amex Blue Cash Preferred — Best for Families

6% at US supermarkets (up to $6K/year) | 6% streaming | 3% transit/gas | $95 annual fee

If you spend $500+/month on groceries, the Blue Cash Preferred pays for itself before you factor in streaming and transit rewards. A family spending $600/month on groceries earns $432/year on that category alone — a net return of $337 after the fee.

Best for: Households with high grocery and streaming spend.

How to Pick the Right Cash Back Card

The right card depends on your spending pattern. Here's a decision framework:

- If your biggest spend is groceries: Amex Blue Cash Preferred

- If your biggest spend is dining out: Chase Freedom Unlimited (or Sapphire Preferred if you also travel)

- If you want simplicity: Citi Double Cash

- If you're just starting out: Chase Freedom Unlimited

The two-card setup that maximizes most people's returns: Chase Freedom Unlimited for dining, drugstores, and travel + Citi Double Cash for everything else. You capture 3% on your highest-margin category and 2% on everything else.

Building Credit While Earning Cash Back

Cash back cards are also your credit-building tool. On-time payments and low utilization (keep balances under 30% of your credit limit, ideally under 10%) are the two biggest drivers of your credit score.

A higher credit score directly translates to lower interest rates on mortgages and auto loans — potentially saving tens of thousands of dollars over your lifetime. The cash back is almost secondary to what consistent credit card use does for your score over 5 years.

Next step: Cash back goes further when it compounds. Deposit your rewards in a HYSA earning 5% →

The AI Money Machine

Cash back is nice — but AI income is better. Build a full revenue engine with the exact methods, scripts, and workflows inside.

$47 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.