Your 30s are the decade when the financial decisions you make in your 20s either start paying off or start costing you. You're likely earning more than you ever have. Your spending may have also increased. The gap between income and wealth accumulation has never been wider — or more important to close.

Here's the framework that actually works.

Free Resource

Your 30s wealth plan starts here.

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →Why Your 30s Are the Critical Decade

Compound interest has a geometric quality that most people only understand abstractly. Let's make it concrete:

- $50,000 invested at 30, growing at 7%, becomes $748K by 65

- $50,000 invested at 40, growing at 7%, becomes $380K by 65

- $50,000 invested at 50, growing at 7%, becomes $194K by 65

The same $50K, invested a decade earlier, is worth almost twice as much at retirement. That's the compounding effect — and it's why your 30s, not your 50s, is when the heavy lifting happens.

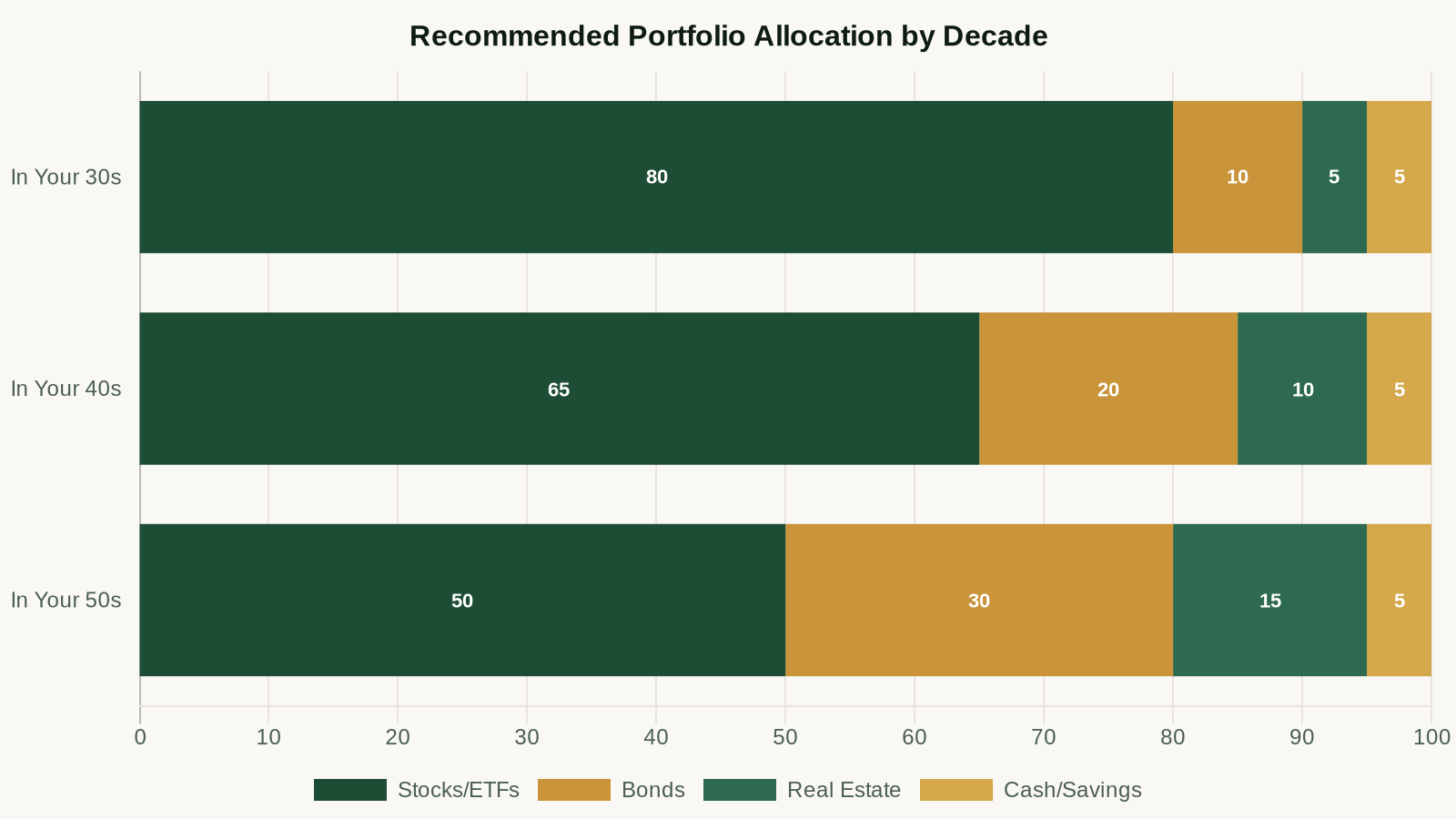

The Wealth-Building Hierarchy: Where to Deploy Capital

The order in which you allocate money matters enormously. Here's the priority stack:

Step 1: Eliminate High-Interest Debt (8%+ APR)

No investment reliably returns more than 8–10% annually. Credit card debt at 20% APR is guaranteed -20% return on every dollar you're not paying down. There is no wealth-building move that beats eliminating this debt first.

Student loans are more nuanced. At 4–6%, they're below your expected investment return. At 8%+, pay them off before investing beyond your employer match.

Step 2: Capture Your Full Employer 401(k) Match

A 100% match on your contributions up to 3% of salary is an immediate 100% return. There is no investment in the world that offers a guaranteed 100% return. Max your match before doing anything else.

Step 3: Build Your Emergency Fund (3–6 Months of Expenses)

An emergency fund isn't a "nice to have" — it's what prevents a $3,000 car repair from becoming $3,000 in credit card debt at 20% interest. Park it in a high-yield savings account earning 5% while it waits.

Step 4: Max Your Roth IRA ($7,000 in 2026)

After your 401(k) match and emergency fund, a Roth IRA is your best next move. Tax-free growth on money you contribute in your 30s will compound for 30+ years. The $7,000 annual contribution may feel significant now, but it becomes the most powerful wealth-building tool you have over time.

Step 5: Increase Your 401(k) Contribution

Aim to max your 401(k) ($23,000 in 2026). If that's not achievable immediately, set a goal to increase your contribution 1% each year until you get there. Automate it to happen when you get a raise so you never feel the reduction.

Step 6: Taxable Brokerage Account

Once tax-advantaged accounts are maxed, open a taxable brokerage account and continue investing. You don't get the tax benefits, but you get liquidity and no contribution limits.

Open a Fidelity Roth IRA — Start Investing Today →

The Income Side: Growing Your Earning Power

Savings rate is powerful, but income growth is what makes the math dramatically easier. In your 30s, this means:

- Negotiate every 2 years — the biggest salary increases come from either negotiating or job-hopping, not from waiting for annual reviews

- Build a skill premium — identify the skill in your industry that commands 20–40% higher compensation and invest in developing it

- Create equity exposure — RSUs, stock options, or a side business that could eventually pay off asymmetrically

The math on income growth: a $20K salary increase invested every year for 20 years at 7% return creates over $820K in additional wealth. A single successful salary negotiation can be worth hundreds of thousands of dollars over a career.

What Most People in Their 30s Get Wrong

Lifestyle inflation that tracks income growth 1:1

Every raise that goes entirely into a bigger apartment, nicer car, or more dining out is a raise you didn't get. The goal is to let your lifestyle grow, but make sure your savings rate grows faster. If you get a 10% raise, spend 5% of it and invest the other 5%.

Treating a house as an investment

A primary residence is not an investment in the financial sense — it's a large, illiquid asset that generates zero cash flow and has ongoing carrying costs. Home appreciation historically tracks inflation. It's a consumption decision with some equity-building, not a wealth-building strategy.

Waiting to invest until they feel "ready"

There is no moment of readiness. Markets will always feel too high or too uncertain. The answer is to invest consistently regardless of market conditions (dollar-cost averaging), hold low-cost index funds, and ignore short-term noise.

A Simplified 30s Wealth-Building Checklist

- ☐ Zero high-interest debt (credit cards, personal loans at 8%+)

- ☐ 3–6 month emergency fund in a HYSA earning 4%+

- ☐ 401(k) contribution capturing full employer match

- ☐ Roth IRA open and contributing annually

- ☐ Savings rate ≥ 20% of gross income

- ☐ No recurring subscriptions that don't deliver clear value

- ☐ Salary reviewed/negotiated in the last 18 months

- ☐ Net worth tracked (even if just a spreadsheet)

You don't need to accomplish all of this by 35. You need a direction. Pick the first item on the list you haven't completed and work on that exclusively until it's done.

Start here: If you don't have a high-yield savings account for your emergency fund, that's your first move. See the best HYSAs →

For automated investing — especially if you want your Roth IRA to manage its own allocations as you age — Betterment is worth a look. Set your target retirement date and it handles rebalancing automatically.

Try Betterment — Automated Investing for the Long Game →

10 Income Streams Blueprint

Build 10 distinct income streams with AI doing the heavy lifting. 42-page system, 30-day plan, done-for-you tracker.

$97 one-time

Keep Reading

Recommended Product

Want to learn how to build 10 income streams?

The 10 Income Streams Blueprint ($97) walks you through the complete framework for building multiple income sources — from side hustles to scalable businesses.

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.