The biggest investing mistake isn't picking the wrong stock. It's waiting. Every year you delay investing is a year of compound interest you can't recover. The good news: the minimum barrier to entry is now effectively zero. You can open a brokerage account, buy fractional shares of a diversified index fund, and start building wealth with $100 or less — today, in about 15 minutes.

Here's exactly how to do it, what to buy, and why starting small is dramatically better than waiting until you have "enough."

Free Resource

Need a step-by-step investing roadmap?

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →Where to Invest $100: Platform Comparison

| Platform | Account Minimum | Fractional Shares? | Best For | Annual Fee |

|---|---|---|---|---|

| Fidelity ⭐ Best Overall | $0 | Yes ($1 minimum) | Long-term index investing | $0 |

| Webull | $0 | Yes | Active traders, research tools | $0 |

| Betterment | $0 | N/A (automated) | Hands-off automated investing | 0.25%/year |

| Robinhood | $0 | Yes | Simple interface, beginners | $0 (Gold: $5/mo) |

The Case for Starting Now with $100

People who wait to invest until they have $1,000 or $5,000 are making a math error. Here's why starting with $100 today beats waiting:

Assume you invest $100/month starting at age 25 versus starting at 35, with a 7% average annual return:

- Starting at 25: $100/month for 40 years = $262,000 at 65

- Starting at 35: $100/month for 30 years = $122,000 at 65

Waiting 10 years to "have more to invest" costs you $140,000 in final value — even though you'd only contribute $12,000 more by starting earlier. That's the compound interest gap, and no amount of future investing recovers it.

What to Buy with $100

When you're starting with $100, the right investment is simple and boring: a broad index fund.

The Best Option: A Total Market Index Fund

A total stock market index fund owns tiny pieces of every publicly traded company in the US. You get instant diversification across thousands of companies with a single purchase. When you buy $100 of a total market index fund, you own fractional shares of Apple, Microsoft, Amazon, and 3,000+ other companies.

At Fidelity, the best options for a first investment:

- FZROX — Fidelity Zero Total Market Index. 0% expense ratio. No minimum. Available only at Fidelity.

- FSKAX — Fidelity Total Market Index. 0.015% expense ratio. Similar coverage.

- VTI (Vanguard) or ITOT (iShares) — Available everywhere, 0.03% expense ratio, same concept.

Buy one of these. Don't overthink it. The fund matters far less than the habit of investing consistently.

Should You Buy Individual Stocks with $100?

No — especially not at the start. Individual stocks carry company-specific risk that diversification eliminates. If you put $100 into a single company and it drops 40% (which individual stocks do, regularly), you've lost $40. If you put $100 into an index fund and the market drops 40%, it's a temporary decline in a diversified position — and history shows it recovers.

Build the index fund habit first. After you have $1,000+ consistently invested, then you can allocate a small amount to individual stock picks if that interests you.

Step-by-Step: Invest Your First $100

- Open a Fidelity account — takes 10–15 minutes. Choose a Roth IRA if you're under the income limit and this is retirement money; choose a taxable brokerage account if it's general investing.

- Transfer $100 from your bank account. It will be available to trade within 2–5 business days (or instantly for some methods).

- Search for FZROX (or VTI/ITOT if you opened elsewhere).

- Click "Buy" and enter "$100" as a dollar amount (fractional shares allow this).

- Set up a recurring investment — even $25/week. Consistent contributions matter more than lump sums.

Account Types: Roth IRA vs. Taxable Brokerage

If you're investing for retirement (money you won't touch for 20+ years), open a Roth IRA first. The tax-free growth is worth more than any minor inconvenience of the retirement account structure. Contribution limit: $7,000/year under age 50 in 2026.

If you're investing for a shorter horizon (5–15 years), or you've already maxed your Roth IRA, use a taxable brokerage account. You'll pay capital gains tax on profits, but you can withdraw the money anytime without penalty.

For most beginners: Roth IRA first, then taxable brokerage once the Roth is maxed.

What Happens After $100

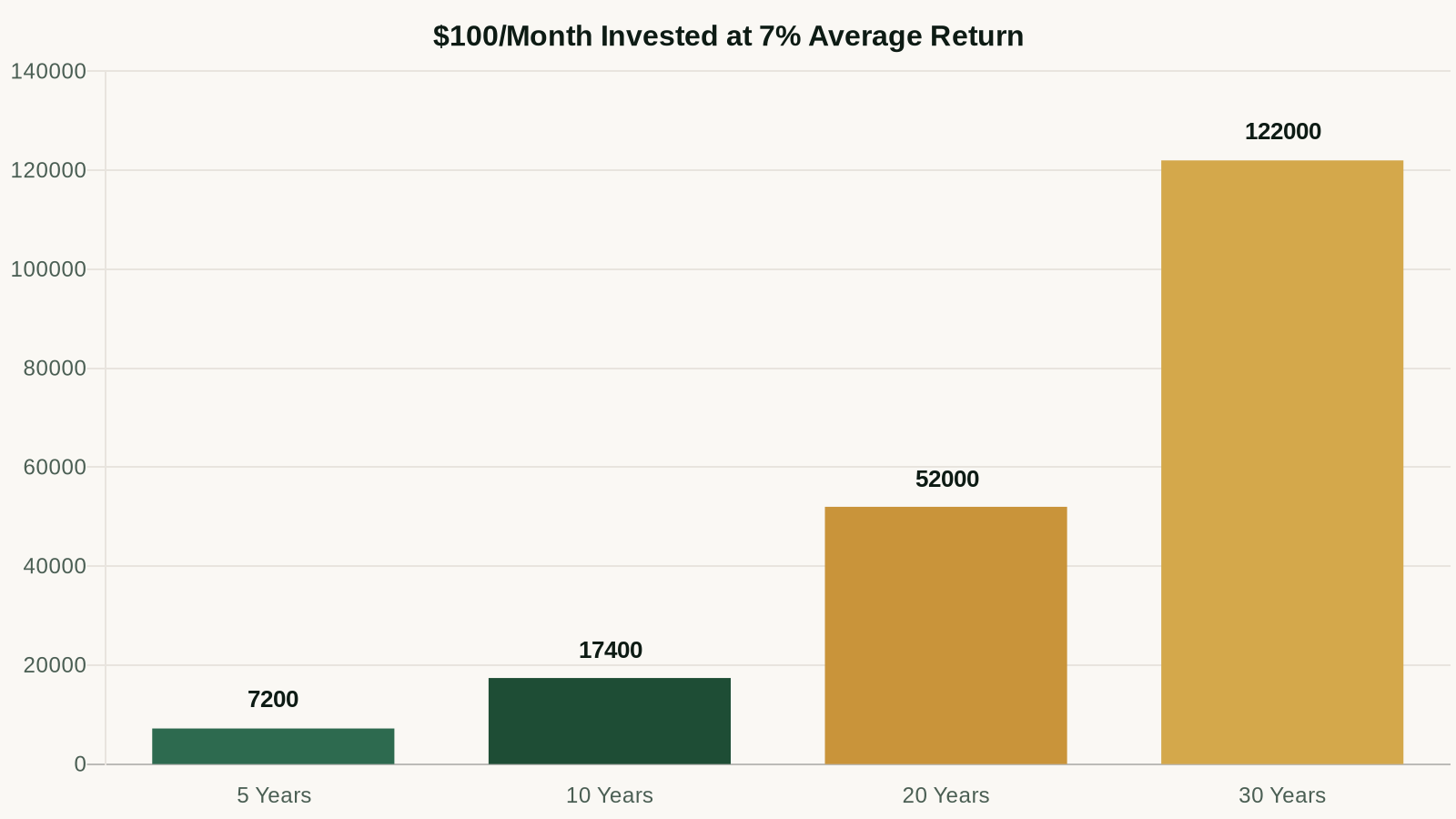

The goal isn't to invest $100 once — it's to build the habit of investing consistently. Here's what the growth looks like:

- $100/month invested for 5 years at 7%: $7,200

- $100/month invested for 10 years at 7%: $17,400

- $100/month invested for 20 years at 7%: $52,000

- $100/month invested for 30 years at 7%: $122,000

Increase your contributions as your income grows. Raise your monthly investment by half of every raise you get. The compounding does the work — you just need to show up consistently.

Frequently Asked Questions

Is it worth investing such a small amount?

Yes — because you're not just investing $100, you're building the habit and the account structure that you'll use for decades. The $100 matters less than the system you're creating.

What if the market drops right after I invest?

That's normal. Markets go up and down. If you're investing for 20+ years, short-term drops are irrelevant — they're actually buying opportunities if you continue investing monthly. Never check your balance daily; check it quarterly at most.

Do I need to pay taxes on my investment gains?

If investing in a Roth IRA: no taxes on gains, ever. If investing in a taxable brokerage account: you pay capital gains tax when you sell. Long-term capital gains (held 1+ year) are taxed at 0%, 15%, or 20% depending on your income — much lower than ordinary income tax rates.

How is a brokerage account different from a savings account?

A savings account holds cash and pays a fixed interest rate. A brokerage account holds investments (stocks, bonds, index funds) whose value fluctuates with the market. Savings accounts are for money you might need soon; brokerage accounts are for money you're growing over years.

10 Income Streams Blueprint

Build 10 distinct income streams with AI doing the heavy lifting. 42-page system, 30-day plan, done-for-you tracker.

$97 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.