The 401(k) vs Roth IRA debate is one of the most common questions in personal finance — and the framing is usually wrong. It's not either/or. For most people, the right answer is both, in a specific order. Get the order wrong and you leave free money on the table or pay unnecessary taxes. Get it right and you're maximizing every dollar you invest for retirement.

Here's the exact framework for deciding where to put your retirement savings in 2026.

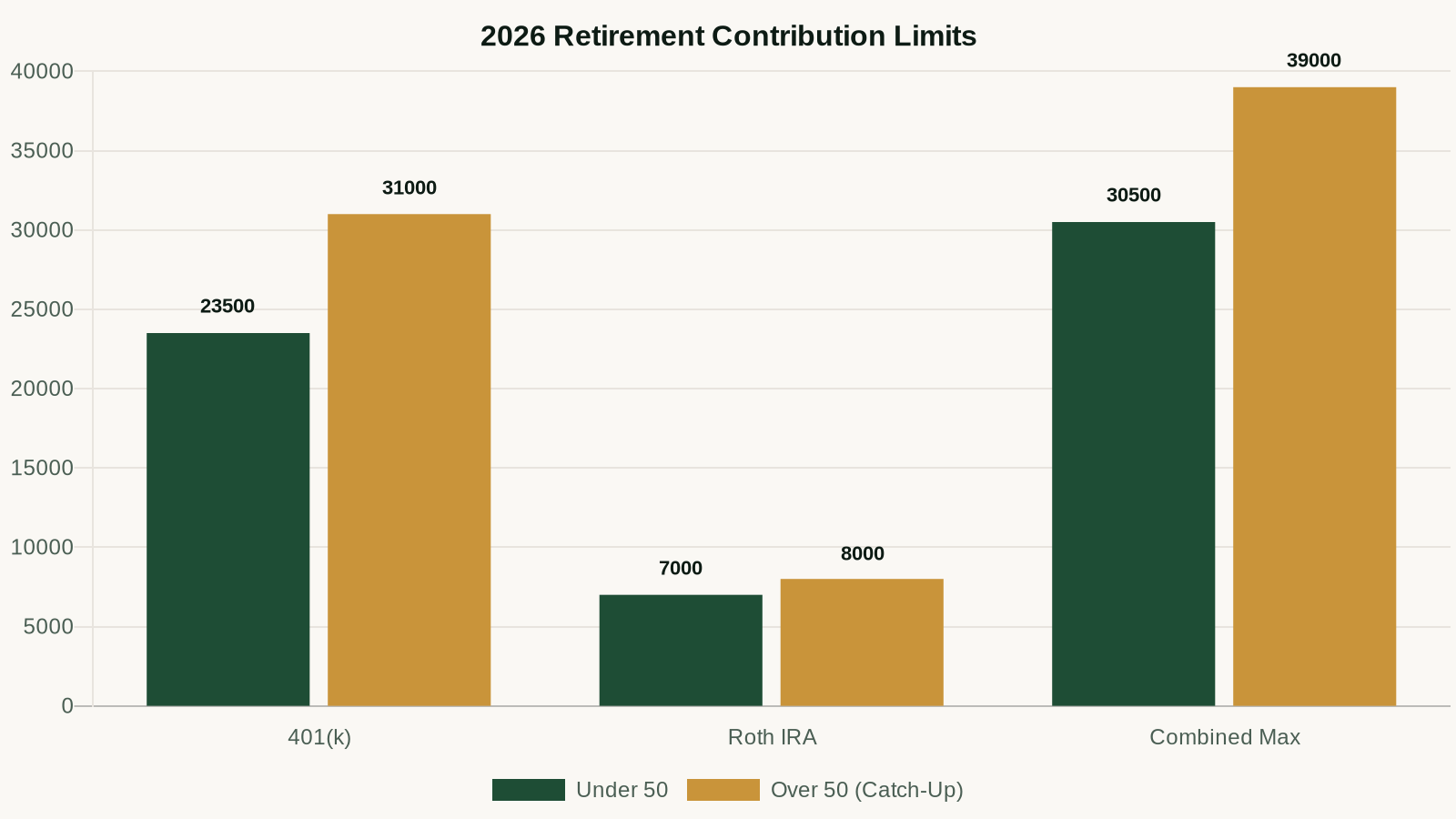

2026 Contribution Limits at a Glance

| Account | 2026 Limit (Under 50) | 2026 Limit (50+) | Tax Treatment | Employer Match? |

|---|---|---|---|---|

| 401(k) — Traditional | $23,500 | $31,000 | Pre-tax now, taxed at withdrawal | Yes (if offered) |

| 401(k) — Roth | $23,500 | $31,000 | After-tax now, tax-free at withdrawal | Yes (if offered) |

| Roth IRA | $7,000 | $8,000 | After-tax now, tax-free at withdrawal | No |

| Traditional IRA | $7,000 | $8,000 | Pre-tax (if deductible), taxed at withdrawal | No |

The Priority Order: Where to Put Your Money First

This is the framework most financial planners use, and it's correct for the vast majority of people:

- 401(k) up to the employer match — this is free money. A 50% match up to 6% of salary is a 50% instant return. Nothing else in personal finance competes with this. Do this first, always.

- Roth IRA up to the annual limit — after the match, the Roth IRA usually beats the 401(k) because of investment flexibility, no required minimum distributions, and the ability to withdraw contributions penalty-free.

- Back to the 401(k) — max it out — once the Roth is maxed, return to the 401(k) and contribute up to the $23,500 limit.

- Taxable brokerage account — if you've maxed both, open a standard brokerage account for additional retirement investing.

Why the Employer Match Comes First

If your employer matches 50 cents on every dollar up to 6% of your salary, and you make $70,000/year, the math is:

- Your 6% contribution: $4,200/year

- Employer match (50%): $2,100/year

- Effective return on that $4,200: 50% instantly

There is no investment anywhere — stocks, real estate, crypto — that guarantees a 50% return. Failing to capture the employer match is the single most expensive mistake in retirement planning.

401(k) vs Roth IRA: The Core Difference

The fundamental difference is when you pay taxes:

- Traditional 401(k): You contribute pre-tax (lowers your taxable income now), pay taxes when you withdraw in retirement. Bet that your tax rate will be lower in retirement.

- Roth IRA: You contribute after-tax (no deduction now), pay zero taxes on growth and withdrawals in retirement. Bet that your tax rate will be higher in retirement — or at least the same.

For most people in their 20s and 30s, the Roth wins. You're in a relatively low tax bracket now, you have decades of tax-free compounding ahead, and you avoid the risk of unknown future tax rates on your retirement withdrawals.

When the Traditional 401(k) Beats the Roth IRA

The 401(k) is the better vehicle when:

- You're in a high tax bracket now (above 32%) and expect to drop significantly in retirement

- You want to reduce your current taxable income to qualify for deductions or credits

- You're over 50 and have less time for compounding to overcome the tax difference

Roth IRA Advantages Beyond the Tax Benefit

The Roth IRA has structural advantages that go beyond just taxes:

- No required minimum distributions (RMDs): Traditional accounts force you to start withdrawing at 73. The Roth doesn't — your money can keep compounding indefinitely.

- Contribution withdrawal flexibility: You can withdraw your contributions (not earnings) from a Roth IRA anytime, for any reason, with no penalty. This makes it a secondary emergency fund of sorts.

- Better investment options: 401(k) plans are limited to the funds your employer chose. A Roth IRA at Fidelity or Betterment gives you access to thousands of low-cost funds.

- Estate planning advantages: Roth IRA heirs don't pay income tax on inherited Roth withdrawals.

Income Limits: Can You Even Use a Roth IRA?

The Roth IRA has income limits. For 2026:

- Single filers: Phase out from $150,000–$165,000 MAGI

- Married filing jointly: Phase out from $236,000–$246,000 MAGI

Above $165,000 (single) or $246,000 (married), you cannot contribute directly. However, you can use the backdoor Roth IRA strategy: contribute to a non-deductible Traditional IRA and immediately convert to a Roth. Consult a tax advisor if you're in the phase-out range.

The Real Answer: Do Both, In Order

The 401(k) vs Roth IRA debate resolves cleanly:

- Capture 100% of your employer match in the 401(k)

- Max your Roth IRA ($7,000 in 2026)

- Return to your 401(k) and increase contributions toward the $23,500 limit

- If still have savings capacity: taxable brokerage account with index funds

The total potential tax-advantaged space in 2026: $23,500 (401k) + $7,000 (Roth IRA) = $30,500/year. Most people can't hit that ceiling and should focus on steps 1 and 2 before worrying about the rest.

Once you've decided to open a Roth IRA, Betterment handles the investment allocation automatically — shifting to more conservative holdings as you approach retirement. No fund picking required.

Open a Betterment Roth IRA — Automated Retirement Investing →

Frequently Asked Questions

Can I contribute to both a 401(k) and a Roth IRA in the same year?

Yes. They have completely separate contribution limits. You can max out your 401(k) at $23,500 AND your Roth IRA at $7,000 in the same calendar year for a total of $30,500 in tax-advantaged retirement contributions.

What if my employer doesn't offer a 401(k) match?

Skip the 401(k) for now and go straight to the Roth IRA. Without the match, the Roth IRA is usually the better vehicle because of its flexibility and investment options. After maxing the Roth, you can contribute to the 401(k) or a SEP-IRA if self-employed.

Should I choose Roth 401(k) or Traditional 401(k)?

If your employer offers a Roth 401(k) option, it's worth considering if you're in the 22% or lower tax bracket. For higher earners (32%+), the Traditional 401(k) tax deduction usually wins. When in doubt, split contributions: 50% to Traditional, 50% to Roth for tax diversification.

What happens to my 401(k) if I leave my job?

You have several options: leave it with the old employer, roll it into your new employer's 401(k), roll it into an IRA (recommended for most people — more investment options), or cash it out (avoid this — you'll pay taxes plus a 10% penalty if under 59½).

10 Income Streams Blueprint

Build 10 distinct income streams with AI doing the heavy lifting. 42-page system, 30-day plan, done-for-you tracker.

$97 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.