If you're carrying high-interest credit card debt, a balance transfer is one of the most powerful tools available for paying it off faster. Transfer your balance to a 0% APR offer, and every payment goes directly toward principal — no interest accruing for 15–21 months. The right balance transfer card can save you $1,000–$3,000+ in interest on a $10,000 balance. Here are the best offers of 2026.

Best Balance Transfer Cards at a Glance

| Card | 0% APR Period | Transfer Fee | Regular APR After | Credit Score Needed |

|---|---|---|---|---|

| Citi Simplicity Card ⭐ Best Overall | 21 months | 3% (min $5) | 19.24–29.99% | Good (670+) |

| Wells Fargo Reflect Card | 21 months | 5% (min $5) | 18.24–29.99% | Good (670+) |

| Discover it Balance Transfer | 18 months | 3% (first 18 months) | 18.24–28.24% | Good (670+) |

| Chase Slate Edge | 18 months | 3% (first 60 days), 5% after | 20.49–29.24% | Good (670+) |

| BankAmericard | 18 months | 3% (first 60 days) | 16.24–26.24% | Good (670+) |

How Balance Transfers Actually Work

A balance transfer moves existing debt from a high-interest card to a new card offering 0% APR for a promotional period. Here's the complete mechanics:

- Apply for the new card: You need good to excellent credit (670+ FICO) to qualify for the best offers.

- Request the transfer: Either during the application process or after approval. You provide the account number and amount to transfer from your existing card.

- Pay the transfer fee: Typically 3–5% of the transferred amount. On a $10,000 balance at 3%, that's $300 upfront.

- 0% APR period begins: From account opening, not from the transfer date. The clock starts immediately.

- Pay it off before the period ends: If you haven't paid the full balance when the promotional period expires, the remaining balance starts accruing interest at the regular APR (often 20–29%).

The Math: How Much Can You Save?

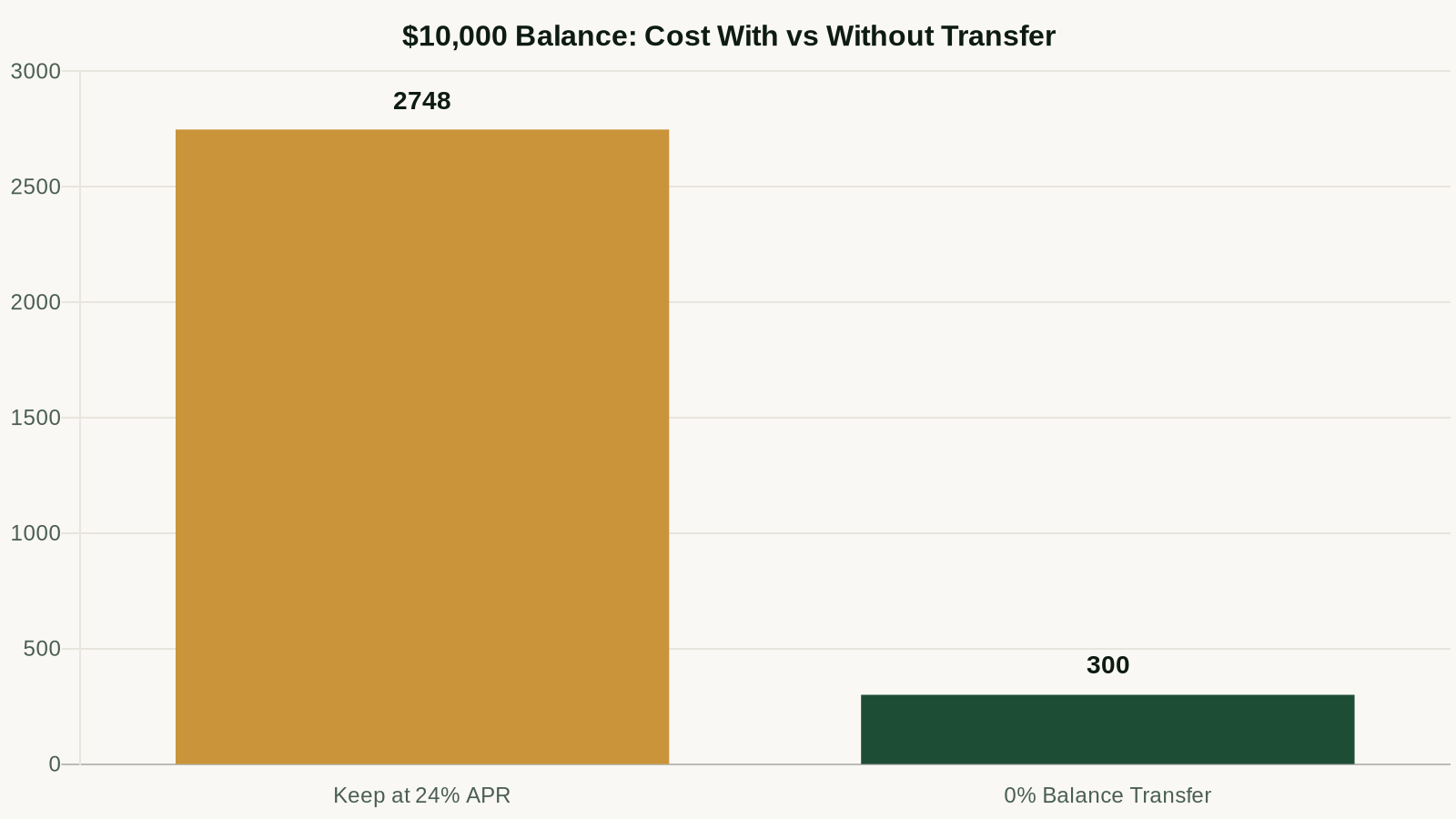

On a $10,000 balance at 24% APR, paying $500/month:

- Without a transfer: Takes 26 months, costs $2,748 in interest

- With a 21-month 0% transfer (3% fee): Pay $300 transfer fee, zero interest for 21 months, save $2,448 net

The math almost always favors the balance transfer when you have high-interest debt and the discipline to pay it down during the promotional period.

Best Balance Transfer Cards: Detailed Reviews

1. Citi Simplicity Card — Best Overall (21 Months, No Late Fees)

The Citi Simplicity stands out for two reasons: 21 months of 0% APR (tied for longest available) and no late fees, which protects you if you occasionally miss the due date without derailing your payoff plan. The 3% transfer fee is standard. No annual fee.

Best for: Anyone with a large balance who needs the maximum time to pay it off.

Limitation: No rewards after the promotional period ends — this is a pure debt-payoff card, not a keeper card long-term.

2. Wells Fargo Reflect Card — Best for Extended Promotional Period

The Reflect offers 21 months base, extendable to 21 months with on-time payments (terms may vary). The 5% transfer fee is higher than Citi, which matters on large balances — $10,000 × 5% = $500 vs. $300 at 3%. Run the math: if you can pay off your balance in 18 months, the Discover card (18 months, 3% fee) may be a better deal.

Best for: People who want maximum time flexibility and have slightly smaller balances where the fee difference is less impactful.

3. Discover it Balance Transfer — Best for Cash Back After Payoff

Discover's 18-month offer with a 3% fee is strong, but the real differentiator is what comes after: Discover matches all cash back earned in your first year. If you're planning to keep using the card after payoff, the rewards structure makes it compelling long-term. 5% cash back in rotating categories (gas, groceries, online shopping) and 1% on everything else.

Best for: People who want to transition the card into a rewards card after the balance is paid off.

Balance Transfer Pitfalls to Avoid

- Missing a payment: Some cards cancel the promotional rate on the first missed payment. Set up autopay for at least the minimum immediately after transfer.

- Not paying off the full balance: If $2,000 remains when the promotional period ends, that $2,000 starts accruing interest at the regular APR immediately. Have a plan to pay everything off before expiration.

- Making new purchases on the transfer card: New purchases may not qualify for the 0% rate, and your payments may be applied to the 0% balance first, leaving new purchases accruing interest. Read the terms carefully.

- Transferring more than you can pay off: Only transfer an amount you're confident you can pay off within the promotional period. $500/month × 21 months = $10,500 max transfer amount at that payment level.

What Credit Score Do You Need?

Most balance transfer cards require good to excellent credit (670+ FICO). If your score is below 670, work on improving your credit score before applying, or consider a debt consolidation loan as an alternative.

If you apply and get rejected, don't apply for more cards immediately — each hard inquiry drops your score. Wait 3–6 months, work on utilization and payment history, then try again.

Not sure what your credit score is right now? Smart Credit shows your score from all three bureaus (Experian, Equifax, TransUnion) and tells you exactly what's holding you back from approval.

Check Your Credit Score Before Applying →

Frequently Asked Questions

Can I transfer a balance from one card to another at the same bank?

No. Banks don't allow balance transfers between their own cards. You can only transfer balances from cards at different banks. So you can't transfer a Chase card balance to another Chase card.

Does a balance transfer hurt my credit score?

Applying for the new card generates a hard inquiry, which temporarily drops your score 5–10 points. However, once the transfer is complete, your credit utilization on the original card drops to zero, which can significantly boost your score. Net effect over 3–6 months is usually positive if you're paying down debt.

What happens if I don't use all of my credit limit for the transfer?

You're only charged the transfer fee on the amount actually transferred. Unused credit limit doesn't cost you anything — and having available credit actually helps your credit score by lowering your overall utilization ratio.

Should I close my old credit card after the transfer?

Generally no. Closing the old card reduces your total available credit (hurting utilization) and shortens your average account age if it's an older card. Leave it open, set a small recurring charge on it (like a $10/month subscription), and pay it off monthly to keep the account active.

The AI Money Machine

Turn AI into a full-time revenue engine. Monetize AI tools across content, consulting, and digital products — zero prior experience needed.

$47 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.