Your credit score is one of the most financially consequential numbers in your life. The difference between a 620 and a 760 credit score on a $350,000 mortgage is approximately $95,000 in additional interest over 30 years. A poor credit score doesn't just hurt your loan applications — it affects your car insurance rates, apartment applications, and sometimes your job prospects. The good news: if your score is lower than it should be, there are specific actions you can take in 30, 60, and 90 days to raise it.

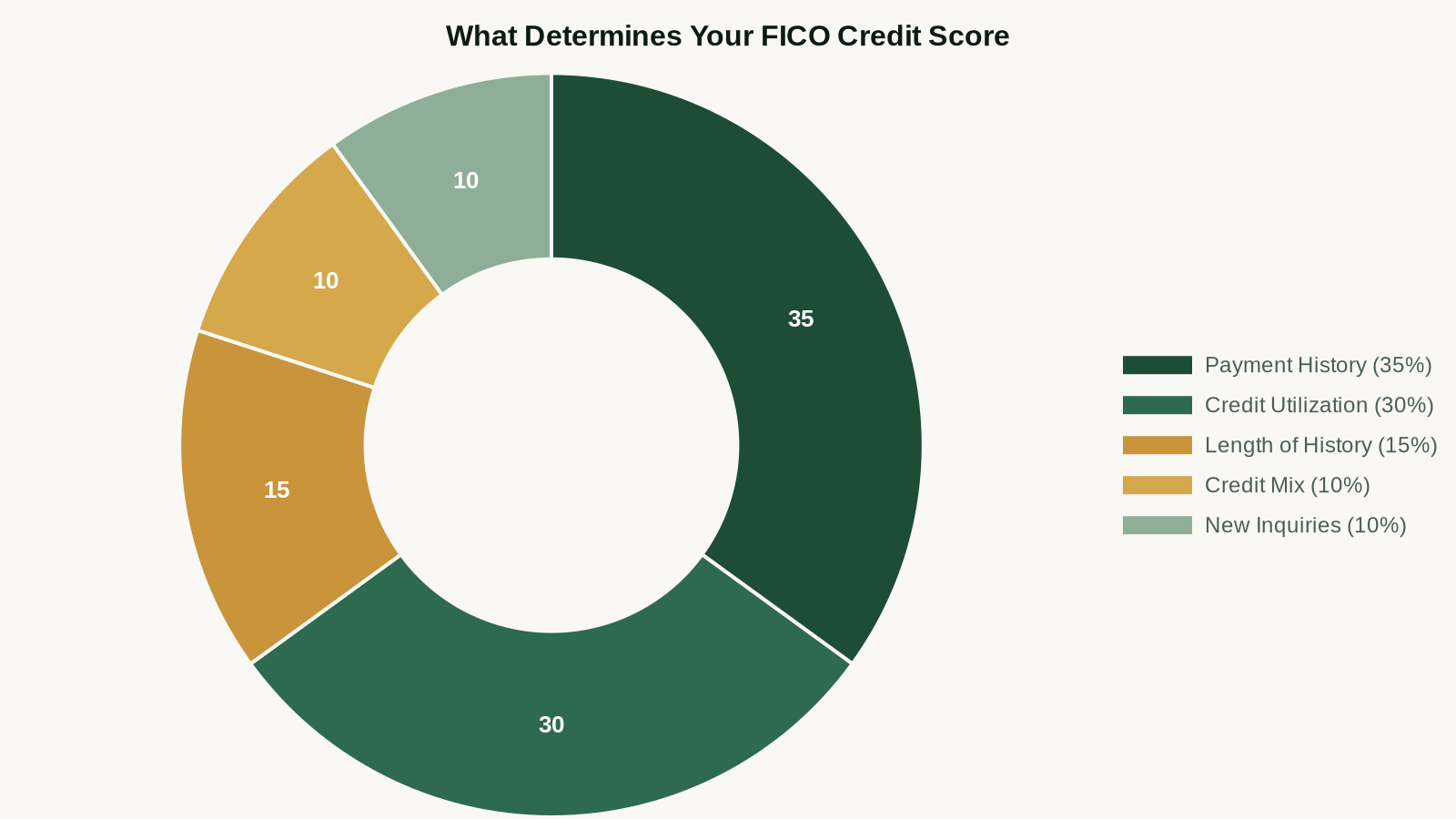

What Determines Your Credit Score

| Factor | Weight in FICO Score | How to Optimize It |

|---|---|---|

| Payment History | 35% | Never miss a payment; use autopay |

| Credit Utilization | 30% | Keep balance below 30% of limit; aim for <10% |

| Length of Credit History | 15% | Keep oldest accounts open; don't close old cards |

| Credit Mix | 10% | Having both revolving and installment credit helps |

| New Credit Inquiries | 10% | Limit hard inquiries; don't apply for multiple cards at once |

30-Day Actions: The High-Impact Moves

These are the fastest-acting changes. Some can show results on your score within a single billing cycle.

1. Pay Down Credit Card Balances (Biggest Impact)

Credit utilization — your balance as a percentage of your credit limit — accounts for 30% of your FICO score and updates every billing cycle. Reducing utilization from 60% to below 30% can raise your score by 20–50 points in as little as 30 days.

The math: if you have a $5,000 credit limit and a $3,000 balance, your utilization is 60%. Paying it down to $1,500 drops utilization to 30%. Paying it to $500 drops it to 10% — which is the target zone for maximum score benefit.

Tactics to find the money:

- Use any savings above your emergency fund minimum

- Redirect next month's discretionary spending

- Sell items you don't need

2. Request a Credit Limit Increase

Increasing your credit limit while keeping your balance the same reduces your utilization ratio instantly. Call your card issuer and request a limit increase — many banks will grant it without a hard inquiry if your account is in good standing. A limit increase from $5,000 to $7,500 with a $1,500 balance drops utilization from 30% to 20%.

Want ongoing credit monitoring so you catch score changes the day they happen? Smart Credit gives you daily credit score updates and personalized action plans for improving your score across all three bureaus.

Monitor Your Credit Score Daily with Smart Credit →

3. Dispute Any Errors on Your Credit Report

Pull your free credit reports from annualcreditreport.com (all three bureaus: Experian, Equifax, TransUnion). Look for:

- Accounts that aren't yours (possible identity theft or reporting error)

- Incorrect late payment marks

- Duplicate accounts

- Accounts showing open that were closed

- Wrong balances or credit limits

Dispute errors directly with the bureau reporting the inaccuracy. Under FCRA, they must investigate within 30 days. Removing an erroneous negative mark can raise your score significantly — sometimes 50+ points.

4. Set Up Autopay for All Accounts

A single 30-day late payment can drop your score 60–100 points and stays on your report for 7 years. Set autopay for at least the minimum payment on every account, then pay the rest manually. This eliminates the risk of a missed payment due to forgetting.

60-Day Actions: Building Momentum

5. Become an Authorized User on a Family Member's Account

If a parent or spouse has a credit card with a long, positive history and low utilization, ask to be added as an authorized user. Their account history can appear on your credit report, improving your average account age and adding a positive payment history. You don't need to use the card — just being on the account helps.

6. Open a Secured Credit Card (If You Have No Credit)

If you have very thin credit history, a secured credit card gives you a reporting account you control. You deposit $200–$500 as collateral, get a matching credit limit, and use it for small purchases you pay off monthly. After 6–12 months of perfect payment history, secured cards typically graduate to unsecured, and the payment history boosts your score significantly.

7. Address Collections Accounts

Collections accounts are major score killers. If you have one, your options:

- Pay-for-delete: Ask the collector to remove the tradeline in exchange for payment. Get the agreement in writing before paying. Not all collectors agree to this.

- Dispute if inaccurate: If the collection is past the statute of limitations or contains errors, dispute it with the credit bureau.

- Wait it out: Collections fall off your report after 7 years. If the collection is more than 5–6 years old, paying it may not be worth it (the mark was already aging off anyway).

90-Day Actions: Structural Improvements

8. Don't Close Old Credit Cards

Closing an old credit card hurts your score in two ways: it reduces your total available credit (increasing utilization) and shortens your average account age (hurting the length of history factor). Keep old cards open even if you don't use them. If there's an annual fee, call and ask to downgrade to a no-fee version.

9. Spread Utilization Across Cards

FICO scores individual card utilization as well as overall utilization. Having one card at 90% utilization hurts more than having all cards at 30%. If you have a high balance on one card, pay it down preferentially — or do a balance transfer to spread the balance across multiple cards.

10. Apply for New Credit Sparingly

Each hard inquiry from a credit application drops your score 5–10 points temporarily. Multiple inquiries in a short period signal credit-seeking behavior to lenders. While you're rebuilding, avoid applying for new credit unless necessary. The exception: mortgage and auto loan inquiries within a 45-day window are treated as a single inquiry.

Realistic Score Improvement Timeline

- 30 days: Pay down utilization, dispute errors. Expect 20–50 point improvement if utilization was high.

- 60 days: Authorized user add, secured card usage. Additional 10–30 points as new positive history starts reporting.

- 90 days: Consistent on-time payments compounding. Score improvement of 40–100+ points from baseline if starting in the 550–620 range.

There is no legitimate way to raise your score 200 points in 30 days. Anyone promising that is running a scam. Real score improvement is 30–100 points over 60–90 days through these specific actions, with sustained improvement over 12–24 months as positive history accumulates.

Tracking your progress is half the battle. Smart Credit shows you your score from all three bureaus, alerts you to new inquiries or derogatory marks, and gives you a clear action plan for what to fix next.

Get Your Credit Score from All 3 Bureaus →

Free Resource

Want a step-by-step to improve your credit score?

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →Frequently Asked Questions

How long does it take for credit score improvements to show up?

Credit card issuers typically report your balance to the bureaus once per month (usually on your statement closing date). Once they report, the bureau updates your score within a few days. So paying down a credit card balance can affect your score within 30–45 days of the payment.

Will checking my own credit score hurt it?

No. Checking your own credit score is a "soft inquiry" and has zero impact on your score. Hard inquiries (when a lender pulls your credit for an application) temporarily drop your score. You can check your own score as often as you want — in fact, monitoring it monthly is recommended.

Can I pay someone to fix my credit?

Credit repair companies charge $50–$150/month to do things you can do yourself for free: dispute errors, negotiate with collectors, write goodwill letters. There is nothing a credit repair company can legally do that you can't do yourself. Save the money and do it directly.

Does carrying a small balance help my credit score?

No — this is a widespread myth. Carrying a balance and paying interest does not improve your score. You get full credit score benefit by paying your statement balance in full each month. The best utilization for score purposes is 1–9% (some small balance reporting, not zero), which you achieve by using the card for small purchases and paying in full.

The AI Money Machine

Turn AI into a full-time revenue engine. Monetize AI tools across content, consulting, and digital products — zero prior experience needed.

$47 one-time

Keep Reading

Recommended Product

Want to learn how to build 10 income streams?

The 10 Income Streams Blueprint ($97) walks you through the complete framework for building multiple income sources — from side hustles to scalable businesses.

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.