Your credit score is a three-digit number that determines the interest rate on your mortgage, car loan, and personal loan — and whether you're approved at all. The difference between a 620 and a 760 score on a 30-year mortgage can cost you six figures in interest. Understanding what the numbers mean, what drives them, and how to improve yours is one of the highest-return financial education investments you can make.

Credit Score Ranges: What Each Level Means

| FICO Score Range | Category | Typical Mortgage Rate Impact | Credit Card Approval |

|---|---|---|---|

| 800–850 | Exceptional | Lowest available rates | Approved for best rewards cards |

| 740–799 | Very Good | Near-best rates, ~0.1–0.3% above exceptional | Approved for nearly all products |

| 670–739 | Good | Competitive rates, ~0.5–1% above very good | Approved for most mainstream products |

| 580–669 | Fair | Higher rates; some lenders decline | Limited to secured or subprime products |

| 300–579 | Poor | Very high rates or no approval | Mostly secured cards only |

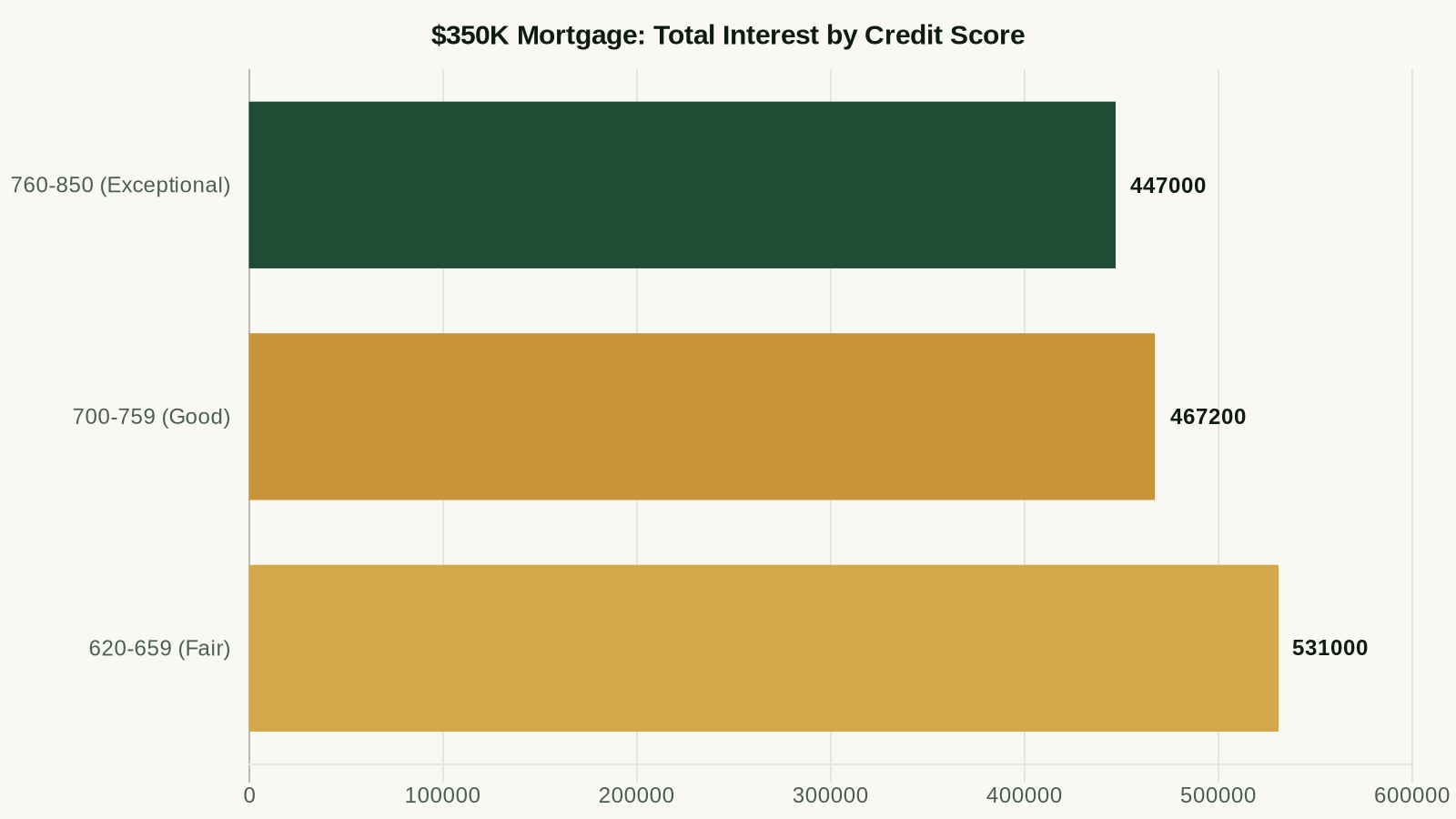

The Real Cost of a Low Credit Score

Credit score differences translate directly into dollar amounts. Here's what a $350,000 30-year mortgage looks like at different score levels (approximate 2026 rates):

- 760–850 (Exceptional): 6.5% rate → $2,212/month → $447,000 in total interest

- 700–759 (Good-Very Good): 6.75% rate → $2,270/month → $467,200 total interest (+$20,200)

- 620–659 (Fair): 7.5% rate → $2,447/month → $531,000 total interest (+$84,000)

A 140-point score difference between "fair" and "exceptional" costs $84,000 on a single mortgage. That's not a hypothetical — that's the real financial cost of a low credit score on the biggest purchase most people ever make.

What Makes Up Your FICO Score

Your FICO score is calculated from five factors, each weighted differently:

1. Payment History (35%)

The single most important factor. Any payment 30+ days late is reported and damages your score for up to 7 years. A single 30-day late payment can drop a 750 score by 60–100 points. Solution: autopay for the minimum on every account, every month, no exceptions. Pay the rest manually, but never miss the minimum.

2. Credit Utilization (30%)

Your total credit card balances divided by your total credit limits. At $3,000 balance across $10,000 total credit, your utilization is 30%. For maximum score benefit, keep utilization below 10% overall and on each individual card. Anything above 30% actively hurts your score.

3. Length of Credit History (15%)

Calculated as the average age of all your accounts plus the age of your oldest account. A 10-year-old credit card contributes significantly to this factor. This is why closing old accounts hurts your score — it removes history and shortens average age.

4. Credit Mix (10%)

Having both revolving credit (credit cards) and installment loans (mortgage, car loan, student loan) slightly improves your score. You don't need to take out loans just to improve your mix — this is a minor factor and shouldn't drive borrowing decisions.

5. New Credit Inquiries (10%)

Each hard inquiry from a credit application drops your score 5–10 points and remains on your report for 2 years (though the score impact fades after 1 year). Apply for new credit sparingly — ideally no more than one new account per 6-month period while building your score.

Before you can improve your score, you need to know exactly where you stand across all three bureaus. Smart Credit gives you daily monitoring, alerts for new inquiries, and a clear breakdown of what's helping and hurting your score right now.

Check Your Score from All 3 Bureaus →

How to Reach 750+ (Step by Step)

If you're starting in the 600–650 range, here's the path to 750+:

- Set autopay on every account — zero missed payments from today forward. Payment history is 35% of your score and takes time to build positive history.

- Pay down credit card balances to below 10% utilization. This is the fastest-acting change — can move the score 30–60 points within 30 days of the card reporting your new lower balance.

- Check your credit reports for errors at annualcreditreport.com. Dispute anything inaccurate. Errors are more common than most people realize — approximately 1 in 5 reports contains an error that could affect the score.

- Keep old accounts open. The oldest account on your report contributes disproportionately to your length of history. Never close your oldest credit card — downgrade to a no-fee version if there's an annual fee.

- Be patient. Negative items age off over 7 years. Late payments from 3 years ago have less impact than fresh late payments. Time is your ally.

How to Build Credit From Zero

If you have no credit history (young adults, recent immigrants), the fastest path:

- Secured credit card: Deposit $200–$500 as collateral, get a matching credit limit, use it for one small purchase monthly, pay it off in full. After 6–12 months, most secured cards graduate to unsecured and return your deposit.

- Become an authorized user: Ask a parent or partner with a long, clean credit history to add you to their account. Their history can appear on your report, instantly adding length and positive payment history.

- Credit-builder loan: Offered by credit unions and some online banks. You make payments into a savings account; once paid off, you receive the funds. The payment history reports to bureaus, building your score.

With these three steps, most people can build a 680+ score within 12–18 months from a zero-history starting point.

Credit Score Myths Debunked

- Myth: Carrying a balance helps your score. False. Paying in full each month is better than carrying a balance. The myth persists because some balance reporting (1–9% utilization) is better than 0% reporting — but this doesn't require carrying a balance that accrues interest.

- Myth: Checking your credit hurts your score. False. Soft inquiries (you checking your own score, pre-approval checks) have zero impact. Only hard inquiries from credit applications affect your score.

- Myth: A higher income means a higher credit score. False. Income doesn't appear in your FICO score calculation at all. A person making $40,000/year can have a better credit score than someone making $200,000/year.

- Myth: Closing paid-off accounts improves your score. Usually the opposite. Closing accounts reduces available credit (raising utilization) and can shorten your average account age.

Track your progress every step of the way. Smart Credit monitors your score daily across Experian, Equifax, and TransUnion and alerts you the moment anything changes — so you always know what's working.

Start Monitoring Your Credit Score Daily →

Frequently Asked Questions

What credit score do I need to buy a house?

The minimum for a conventional mortgage is typically 620, but you won't get competitive rates below 740. FHA loans allow scores as low as 500 (with 10% down) or 580 (with 3.5% down), but you'll pay mortgage insurance. For the best mortgage rates in 2026, aim for 760+.

How often does my credit score update?

Credit issuers typically report to bureaus monthly (usually on your statement closing date). Once the bureau receives updated information, your score recalculates — usually within 1–5 days of the report. If you pay down a card balance, expect to see the score change within 30–45 days.

Which credit score matters — FICO or VantageScore?

FICO is used by approximately 90% of lending decisions in the US, so it's the one that matters most. VantageScore (used by Credit Karma and most free monitoring services) gives you a good approximate sense of your credit health but may differ from your actual FICO score by 20–40 points in either direction.

What's the fastest way to improve credit score by 100 points?

A 100-point improvement is realistic if you're starting below 650 and take the right actions: (1) pay off credit card balances to under 10% utilization, (2) dispute and remove errors from your report, and (3) get added as an authorized user on a long-standing account. These three actions in combination can produce a 50–100+ point improvement within 60–90 days. See our full guide to raising your score fast.

The AI Money Machine

Turn AI into a full-time revenue engine. Monetize AI tools across content, consulting, and digital products — zero prior experience needed.

$47 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.