The average American household carries $7,951 in credit card debt. At a 24% average APR, that's over $1,900/year in interest — money that's generating zero value for you and enormous value for the credit card company. Getting out of debt isn't complicated, but it requires a method, a minimum monthly commitment, and the discipline to execute for months or years. Here's the complete guide to both primary debt payoff strategies.

The Two Methods: Quick Overview

| Method | Order of Payoff | Total Interest Saved | Psychological Benefit | Best For |

|---|---|---|---|---|

| Debt Avalanche | Highest interest rate first | Most (mathematically optimal) | Lower — wins take longer | People motivated by math and maximizing savings |

| Debt Snowball | Smallest balance first | Less (but often close) | Higher — quick early wins | People who need motivation and visible progress |

The Debt Avalanche Method

The avalanche method prioritizes paying off the highest-interest-rate debt first, regardless of balance size. Here's how to implement it:

- List all debts with their balances, interest rates, and minimum payments

- Pay the minimum on every debt every month — no exceptions

- Direct all extra money toward the debt with the highest interest rate

- When the highest-rate debt is paid off, take its entire monthly payment and redirect to the next highest-rate debt

- Repeat until all debts are eliminated

Avalanche Example

Suppose you have three debts and $800/month to allocate:

- Credit Card A: $8,000 balance, 24% APR, $200 minimum

- Credit Card B: $3,000 balance, 19% APR, $75 minimum

- Personal Loan: $5,000 balance, 12% APR, $150 minimum

Minimum payments total $425. Extra monthly budget: $375. In avalanche order, all $375 extra goes to Credit Card A (24% APR) first.

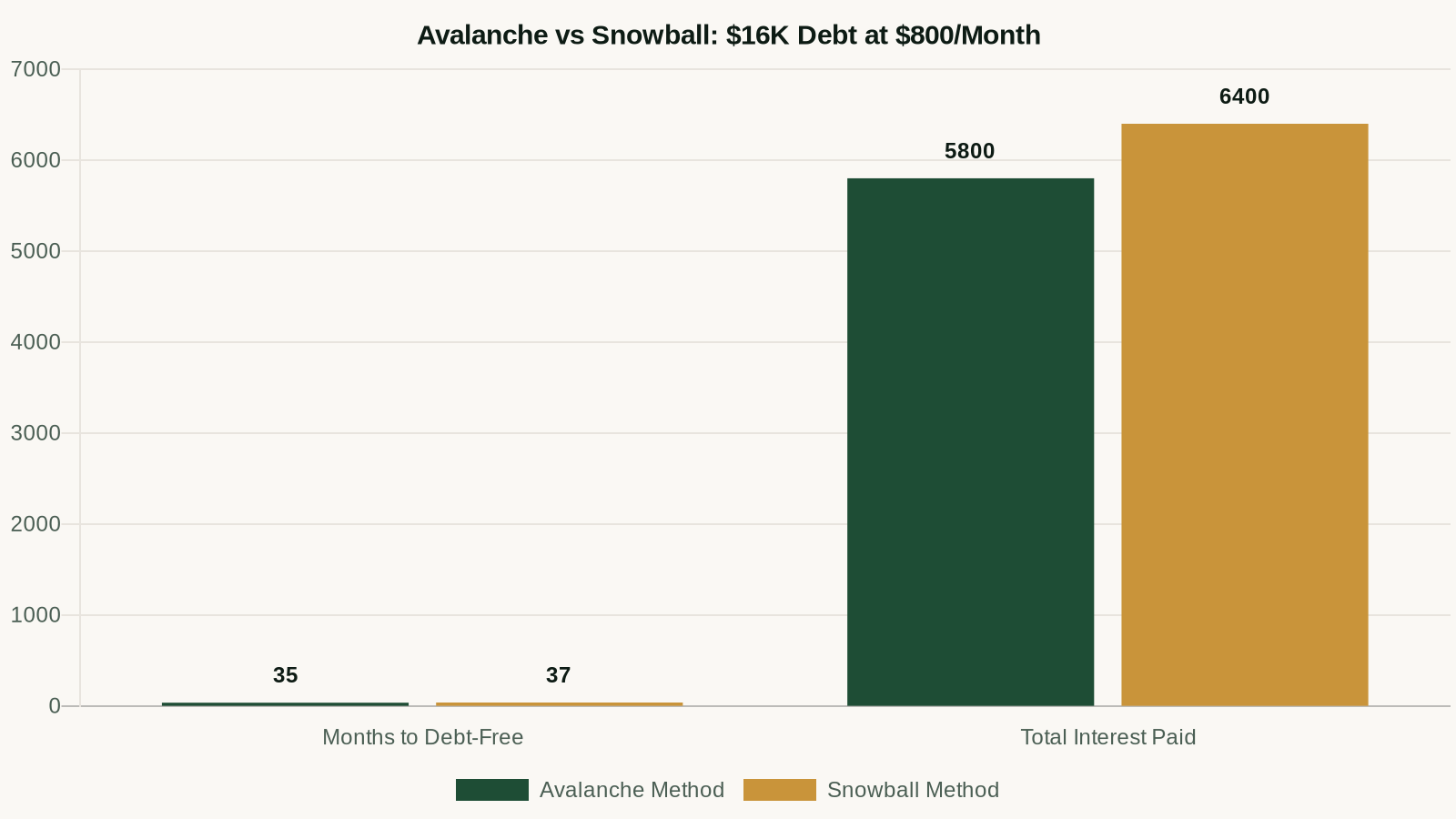

Result: Credit Card A is paid off in ~26 months. All that payment ($575) then attacks Credit Card B. Credit Card B paid off in ~4 more months. Personal loan paid in ~5 more months. Total time: ~35 months. Total interest paid: approximately $5,800.

The Debt Snowball Method

The snowball method prioritizes the smallest balance first, regardless of interest rate. The mechanics are identical to the avalanche — minimum on everything, all extra toward one debt — but the target is different.

Snowball Example

Same three debts, same $800/month budget. In snowball order, all extra goes to Credit Card B first (smallest balance: $3,000):

- Credit Card B ($3,000) is paid off first — in about 7 months

- That payment ($450) then attacks the personal loan ($5,000)

- Personal loan paid off in ~9 more months

- Full force ($800) attacks Credit Card A ($8,000)

- Total time: ~37 months. Total interest paid: approximately $6,400.

The snowball costs $600 more in interest and takes 2 months longer. But you've paid off two accounts within the first 16 months, which provides strong psychological momentum to stay on track.

Which Method Should You Use?

The mathematically correct answer is always the avalanche. But personal finance is personal — and the best strategy is the one you'll actually stick to for 2–3 years.

Research on debt payoff behavior shows that people who use the snowball method are more likely to fully pay off their debt, even though the avalanche would have cost them less. Behavioral economics matters: seeing accounts close provides motivation that abstract interest savings don't.

Choose the avalanche if:

- You're strongly motivated by numbers and can stay focused without quick wins

- The interest rate differences between your debts are large (e.g., 24% vs. 8%)

- Your highest-rate debt also happens to be a smaller balance

Choose the snowball if:

- You've tried to pay off debt before and lost motivation

- You have several small debts that would be paid off quickly

- The interest rate differences are small (all debts within 3–5% of each other)

How to Find the Extra Money

Both methods require extra monthly cash beyond minimums. Finding it requires one or more of these approaches:

Reduce Expenses (Fastest Impact)

- Audit subscriptions — most people have $80–$150/month in unused subscriptions

- Reduce dining out by 2–3 meals/week: saves $150–$300/month for most households

- Temporarily pause retirement contributions above the employer match

- Shop car and home insurance annually — can save $200–$800/year

Increase Income (Higher Ceiling)

- Ask for a raise — the average raise in a job change is 10–20%

- Freelance work in your field on evenings/weekends

- Sell unused items (electronics, furniture, clothing)

- Direct 100% of bonuses and tax refunds toward debt

As you pay down debt, your credit score will improve — but you won't see it if you're not monitoring it. Smart Credit tracks your score across all three bureaus daily and shows you exactly how each debt payoff is affecting your score in real time.

Track Your Score As You Pay Off Debt →

Accelerating the Timeline: Balance Transfers

While executing either method, consider whether a balance transfer to a 0% APR card makes sense. Moving your highest-rate debt to a card with 21 months of 0% interest means every payment goes to principal during that period — dramatically accelerating payoff. The 3% transfer fee is almost always worth it on high-interest balances.

What to Do After You're Debt-Free

Once the last debt is paid, redirect the entire monthly debt payment into:

- Fill your emergency fund to 6 months if not already there

- Max your Roth IRA ($7,000/year)

- Increase 401(k) contributions toward the $23,500 limit

- Build a taxable investment account

The monthly cash flow you were using for debt payments becomes your wealth-building engine. Keeping the same payment discipline you used to get out of debt, but directing it toward investments, is one of the most reliable paths to financial independence.

Once you're debt-free and building credit, keep track of the progress. Smart Credit shows your score from all three bureaus daily, so you see every improvement as it happens.

Monitor Your Credit Score for Free →

Frequently Asked Questions

Should I stop investing while paying off debt?

Capture your employer's 401(k) match first — that's a guaranteed 50–100% return that beats any interest rate. Above the match, it depends on the interest rate: if debt is above 7%, pay it off before investing more. Below 7%, doing both simultaneously often makes sense.

What if I can only afford the minimums right now?

Pay every minimum, every month — no missed payments. Then find even $50–$100 extra to direct toward the target debt. Small extra payments compound over time. A $50 extra monthly payment on a $5,000 balance at 24% APR saves about $1,200 in interest compared to minimums only.

Does paying off debt improve my credit score?

Yes. Paying off revolving debt (credit cards) improves your credit utilization ratio, which can raise your score significantly. Paying off installment debt (loans) has a more modest effect. Either way, you're eliminating monthly payments and freeing cash flow for building wealth.

Is debt consolidation a good idea?

A debt consolidation loan can make sense if you can get a lower interest rate than your current debts and have the discipline not to run up the credit cards again after consolidating them. If consolidation means 12% instead of 24%, and you close the credit cards after paying them off, it can significantly reduce total interest. The risk: many people consolidate and then accumulate new credit card debt, ending up worse off.

The AI Money Machine

Turn AI into a full-time revenue engine. Monetize AI tools across content, consulting, and digital products — zero prior experience needed.

$47 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.