An emergency fund is not a financial goal — it's the foundation that makes every other financial goal possible. Without one, a single car repair or medical bill can unravel months of investing and debt payoff progress. With one, you absorb life's curveballs without touching your investments or adding to your credit card balance.

The standard advice is 3–6 months of expenses. Here's how to calculate your actual number, where to keep the money, and how to build it systematically even if you're starting from zero.

Free Resource

Need a roadmap to build your emergency fund faster?

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →How Much Do You Actually Need?

The "3–6 months" rule is a starting point, not a final answer. Your specific target depends on your situation:

| Situation | Recommended Target | Reasoning |

|---|---|---|

| Dual income, stable jobs, no dependents | 3 months | Lower risk profile; two incomes provide buffer |

| Single income, or variable income | 6 months | Standard target for most households |

| Self-employed, freelance, or commission-based | 6–9 months | Income volatility requires larger cushion |

| Single income, dependents, health issues | 9–12 months | Higher stakes if income disappears |

Calculate Your Actual Monthly Expenses

Don't use your income as the baseline — use what you actually spend. Add up these categories for a true monthly number:

- Housing: Rent or mortgage, property taxes, HOA

- Utilities: Electricity, gas, water, internet, phone

- Food: Groceries and essential dining (not discretionary)

- Transportation: Car payment, insurance, gas, or transit

- Insurance: Health, life, renters/homeowners

- Minimum debt payments: Credit cards, student loans, etc.

- Childcare or dependent care: If applicable

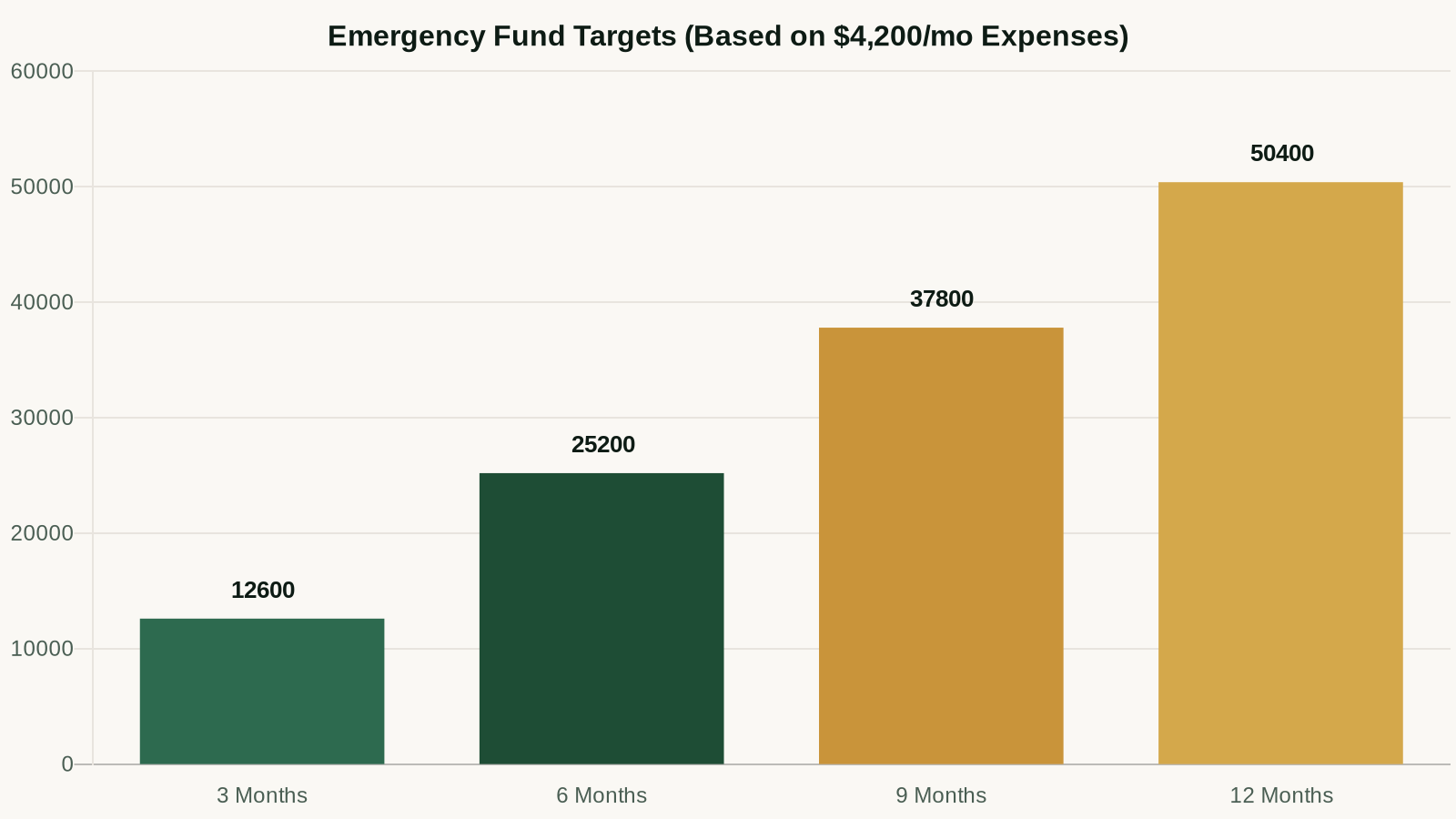

If your essential monthly expenses are $4,200, your 6-month target is $25,200. That's your number. Write it down.

Where to Keep Your Emergency Fund

Your emergency fund needs to be liquid (accessible within 1–2 days), safe (FDIC insured), and earning a meaningful rate. The answer is a high-yield savings account — not your checking account, not the stock market, not a CD with a penalty for early withdrawal.

Why Not Invest Your Emergency Fund?

This comes up constantly. The argument: "I could earn 10% in the market instead of 5% in a HYSA." The problem: the stock market can drop 30–40% right when you need the money most — during a recession, which is exactly when job losses happen. You can't afford a market dip wiping out 30% of your emergency fund the month you get laid off.

The opportunity cost of keeping $25,000 in a HYSA at 5% instead of the market is real — roughly $1,250/year on average. That's the insurance premium you pay for financial stability. It's worth it.

Our top picks for emergency fund storage:

- SoFi High-Yield Savings — 5.10% APY, no fees, FDIC insured up to $2M

- Marcus by Goldman Sachs — 4.90% APY, no minimums, clean interface

- Ally Bank — 4.75% APY, excellent mobile app, full banking ecosystem

Open a SoFi High-Yield Savings Account →

How to Build Your Emergency Fund: A Step-by-Step Plan

Building a 6-month fund feels overwhelming when you're starting from zero. Break it into phases:

Phase 1: Build a $1,000 Starter Emergency Fund (Weeks 1–4)

Before you tackle the full 6-month target, get to $1,000 as fast as possible. This starter fund handles most common emergencies (car repair, minor medical, appliance replacement) and prevents you from going back into debt. To get there fast:

- Pause non-essential subscriptions temporarily

- Sell unused items (Facebook Marketplace, eBay, Craigslist)

- Direct any windfall money (tax refund, bonus, gift) here first

- Pick up extra hours or a side gig for one month

Phase 2: Reach 1 Month of Expenses

Once you have $1,000, set a specific monthly savings target to reach one full month of expenses. Open your HYSA now — don't wait until you have the full amount. Set up an automatic transfer from your checking account the day after payday. Even $200/month adds up: at $200/month you reach one month of expenses ($4,200) in just over 18 months, but most people can go faster once the habit is set.

Phase 3: Scale to 3–6 Months

After one month, the hardest part is done psychologically. Continue the automatic transfers and increase them when possible — raises, eliminated subscriptions, paid-off debts. Use a budgeting app to track progress and find extra savings.

What Counts as an Emergency?

This is where most people go wrong. An emergency fund is for genuine emergencies — unexpected, necessary, urgent expenses. It is NOT for:

- Planned expenses you forgot to budget for (holidays, annual car registration)

- Discretionary upgrades (new phone, vacation)

- Investment "opportunities"

Legitimate emergencies:

- Job loss or major income reduction

- Medical or dental emergency

- Car breakdown required for commuting

- Essential home repair (heat, plumbing, roof leak)

- Emergency travel (family crisis)

If you're unsure whether to use it, wait 48 hours. If it still feels like a genuine emergency then, it probably is.

What to Do After You Use Your Emergency Fund

If you dip into your emergency fund, treat replenishing it as your top financial priority — ahead of extra debt payments and additional investing. Temporarily redirect savings toward restoring the fund to its target level. A partially depleted emergency fund is still vulnerable; get it back to full as quickly as possible.

Frequently Asked Questions

Should I pay off debt before building an emergency fund?

Build a $1,000 starter fund first, even if you have high-interest debt. Without any buffer, unexpected expenses will go straight back onto credit cards, undoing your debt payoff progress. Once you have $1,000, focus on high-interest debt (above 7%), then come back to build the full 3–6 months.

Can I use a Roth IRA as an emergency fund?

Technically you can withdraw Roth IRA contributions (not earnings) without penalty at any time. But this is a bad idea: you lose years of tax-free compounding, the money takes days to settle and transfer, and it conflates two different financial tools. Keep your emergency fund in a HYSA and your retirement money in retirement accounts.

What if I can't save much each month?

Start with whatever you can — even $25/week adds up to $1,300 in a year. The habit matters more than the amount when you're starting. Increase contributions whenever your income grows or expenses drop. See our guide to saving $10,000 in a year for specific tactics.

Should I keep my emergency fund separate from my regular savings?

Yes. Keeping it in a dedicated account (ideally at a different bank than your checking account) prevents accidental spending and makes the balance psychologically clear. Name the account "Emergency Fund Only" if your bank allows it — the label helps.

Budget Blueprint Kit

Zero-to-surplus budgeting done in an afternoon. PDF guide, auto-calculating Excel tracker, and AI prompt library included.

$27 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.