Saving $10,000 in one year sounds like a lot until you break it down: it's $833/month, $192/week, or $27/day. At a median US household income of $78,000 ($5,200/month after taxes), saving $833 requires allocating 16% of take-home pay. That's achievable — but it requires a plan, not willpower.

This guide gives you the specific framework: where to find the money, where to put it, and how to stay on track for 12 months. No gimmicks, no "skip your latte" advice.

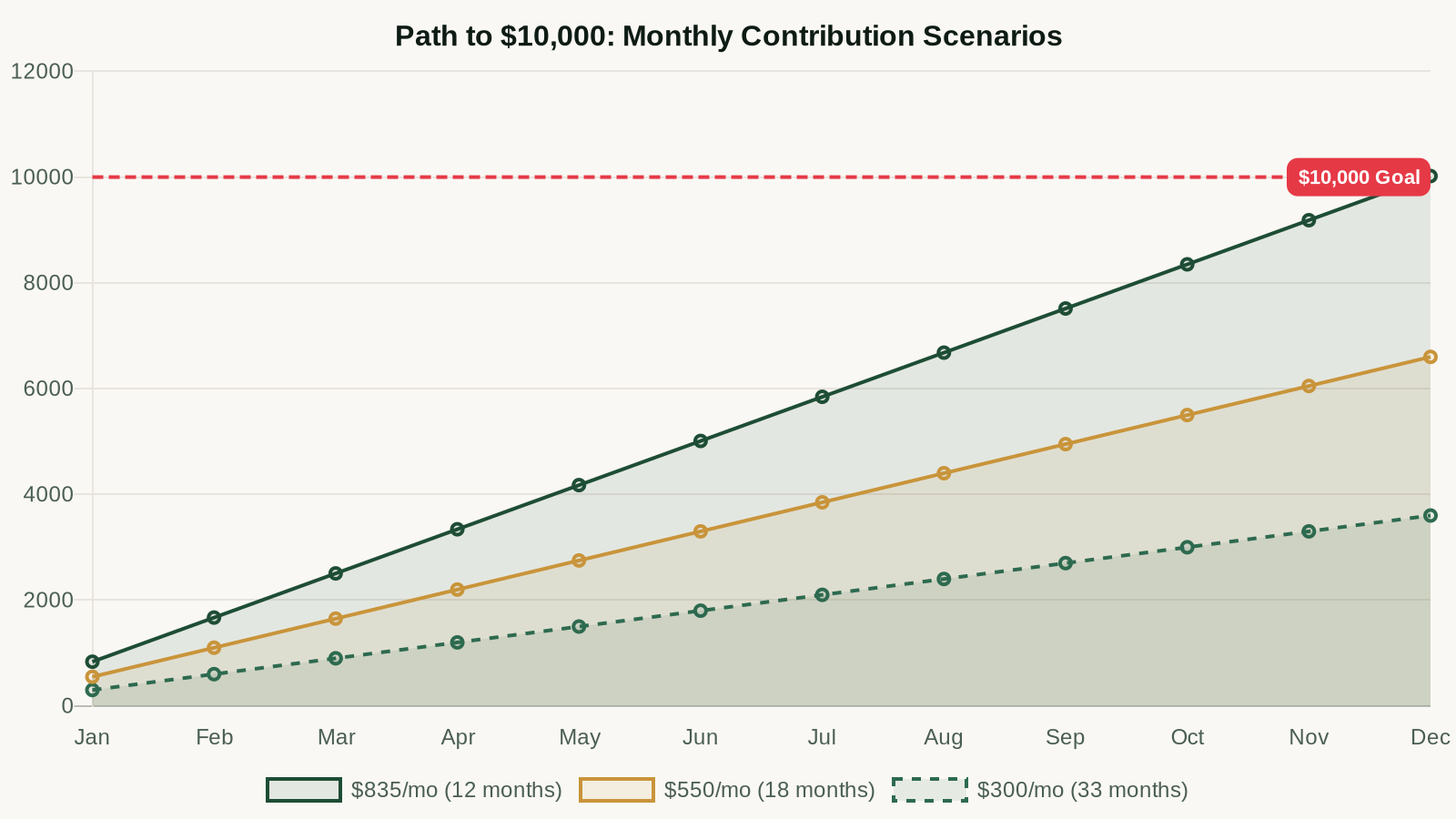

The Math: What $10,000 Actually Requires

| Savings Rate | Monthly Required | Take-Home Needed to Hit 16% | Annual Salary Equivalent |

|---|---|---|---|

| 10% savings rate | $833 | $8,330/month | ~$130,000 |

| 16% savings rate | $833 | $5,200/month | ~$78,000 (median) |

| 20% savings rate | $833 | $4,165/month | ~$63,000 |

| 25% savings rate | $833 | $3,332/month | ~$50,000 |

If your take-home is below $5,200/month, $10,000 in 12 months requires a savings rate above 16%. That's harder but not impossible — especially if you combine expense reduction with income increases. The table above shows that at $63,000 income, a 20% savings rate gets you there. That's achievable.

Step 1: Set Up the Infrastructure First

Before changing a single spending habit, set up the system that makes saving automatic:

- Open a dedicated HYSA for this goal — not your regular savings account. Separation prevents casual spending. SoFi at 5.10% APY is the best option: your $10,000 earns roughly $272 in interest over the year.

- Set up automatic transfer for the day after payday. If payday is the 1st and 15th, your transfer goes out on the 2nd and 16th. This happens before you see the money in checking.

- Name the account "10K Goal 2026" or similar. Named accounts have significantly higher follow-through in behavioral finance research.

Step 2: Find the $833/Month

For most people, $833/month requires a combination of expense cuts and income additions. Start with expenses — they're faster to implement.

The Big Three Expense Categories Worth Cutting

Personal finance research consistently shows that three categories account for most discretionary spending leakage: food, subscriptions, and unused services. Start here:

Food (potential savings: $200–$400/month)

- Drop restaurant spending from 4–5x per week to 1–2x: saves $150–$300/month for most households

- Meal prep Sunday for weekday lunches: saves $50–$100/month vs. daily takeout

- Grocery shopping with a list and no hunger: saves $30–$50/month on impulse buys

Subscriptions (potential savings: $100–$250/month)

- Audit everything: run your bank statement through a subscription tracker in your budgeting app

- Cancel anything unused in the last 30 days

- Downgrade or share plans (streaming services, Spotify, etc.)

- Most people find $80–$150/month in forgotten subscriptions in the first pass

Transportation (potential savings: $100–$200/month)

- Refinance car loan if rates have dropped since you bought (saves $50–$150/month)

- Shop car insurance annually — rates vary by $800+/year for identical coverage

- Reduce rideshare usage if you have a car

Add Income When Expense Cuts Aren't Enough

If cuts alone don't close the gap, income additions are the faster path. One-time income sources to front-load savings:

- Tax refund: Average US tax refund is $3,030 in 2026. Direct it entirely to the 10K account — that's 30% of your goal in one deposit.

- Sell unused items: Electronics, clothing, furniture, sports equipment. Aim for $500–$1,000 in the first 60 days.

- Work bonus or overtime: If available, direct 100% to savings before it hits your lifestyle.

- Side income: Freelance work, tutoring, gig economy shifts. Even 4 hours/week at $25–$35/hour is $400–$560/month extra.

The Month-by-Month Breakdown

Here's how a realistic $10,000 savings year plays out:

- Month 1–2: Set up HYSA, automate $400/month transfer, audit subscriptions, reduce dining out. Target: $1,000–$1,200 saved.

- Month 3: Tax refund hits. Drop $2,000–$3,000 directly into the account. Target cumulative: $4,000–$5,000.

- Month 4–6: Increase automatic transfer to $600/month now that subscription cuts are live. Target cumulative: $6,000–$7,000.

- Month 7–9: Sell unused items, pick up extra income if behind. Target cumulative: $8,000–$8,500.

- Month 10–12: Final push — redirect any extra income, skip a vacation, attack the last gap. Target: $10,000+.

How to Stay on Track for 12 Months

Most savings goals fail not because the math is wrong but because motivation drops after month 3. Prevention tactics that work:

- Track publicly: Tell one person your goal and share monthly updates. Accountability dramatically improves follow-through.

- Celebrate milestones: $2,500, $5,000, $7,500, $10,000. Small, inexpensive celebrations reward progress without derailing savings.

- Never miss twice: If you miss a month's target, double down the next month — not by cutting everything, but by finding one specific thing to add. Missing once is a setback. Missing twice is a pattern.

- Automate as much as possible: The goal is to remove willpower from the equation entirely. Automatic transfers, automatic bill pay, automatic investment contributions all reduce decision fatigue.

Where to Put the $10,000 Once You Have It

The destination depends on the goal:

- Emergency fund: Leave it in the HYSA. It's already there earning 5%+.

- Down payment (3–5 years out): Move to a CD ladder for higher guaranteed returns.

- Investment seed money (5+ year horizon): Fund a Roth IRA ($7,000 for 2026) and put the remainder in a taxable brokerage.

- High-interest debt payoff: Pay off the debt entirely — the guaranteed "return" on eliminating 20% APR debt beats any savings account.

Frequently Asked Questions

What if I can't save $833/month right now?

Set a smaller target — $5,000 or $7,500 — and work up to $10,000 over 18 months instead of 12. The infrastructure (dedicated HYSA, automatic transfers) is more important than the exact number. Consistent saving at $400/month beats sporadic saving at $833/month every time.

Should I pause investing to save $10,000 faster?

Don't pause employer 401(k) contributions up to the match — that's a 50–100% instant return. You can pause above-the-match contributions temporarily. Don't touch existing investments to fund a savings goal unless you're eliminating high-interest debt.

How much interest will I earn during the savings year?

At SoFi's 5.10% APY on an average balance of ~$5,000 during the year, you'll earn roughly $255 in interest. That's not nothing — it's a free $255 toward your goal just for using the right account.

Is it better to pay off debt or save $10,000?

Pay off debt with interest rates above 7% first. Below 7%, saving and paying off debt simultaneously makes sense — you're building a safety net (which prevents future debt) while reducing your existing obligations. Never carry a credit card balance while trying to build savings.

Budget Blueprint Kit

Zero-to-surplus budgeting done in an afternoon. PDF guide, auto-calculating Excel tracker, and AI prompt library included.

$27 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.