Certificates of deposit are having a moment. After years of near-zero rates, the best CDs in 2026 are paying 5%+ on terms as short as 6 months — locking in rates that high-yield savings accounts can cut at any time. If you have cash you won't need for 6–24 months, a CD is worth a serious look.

We compared rates, minimum deposits, and early withdrawal penalties across 15 banks and credit unions. Here's where to get the best return on your locked-up cash.

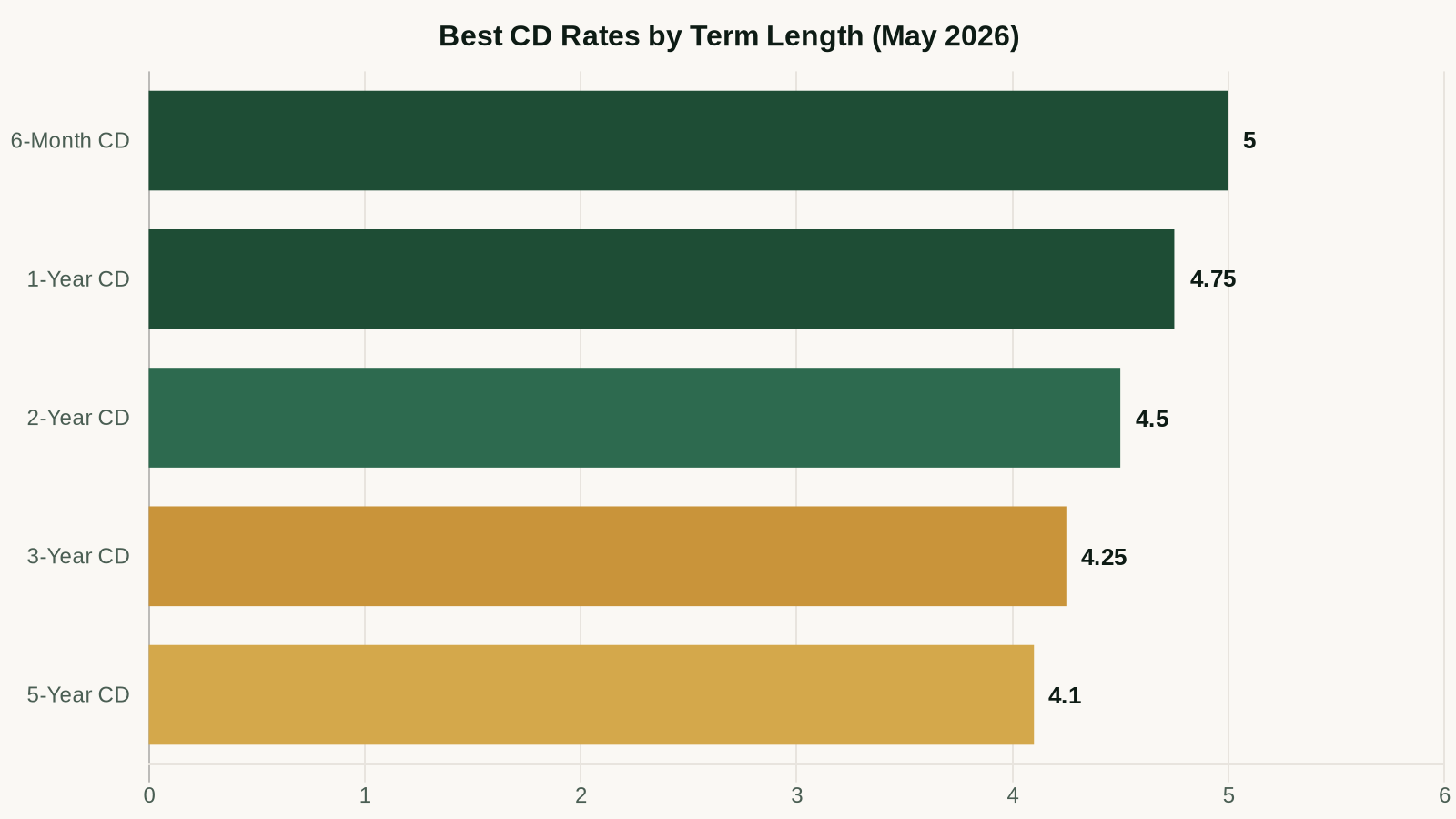

Best CD Rates at a Glance

| Bank | Term | APY | Minimum Deposit | Early Withdrawal Penalty |

|---|---|---|---|---|

| Marcus by Goldman Sachs ⭐ Best 1-Year | 12 months | 5.30% | $500 | 270 days interest |

| Ally Bank | 12 months | 5.20% | $0 | 150 days interest |

| SoFi | 6 months | 5.15% | $500 | 90 days interest |

| Discover Bank | 18 months | 5.00% | $2,500 | 18 months interest |

| Ally No-Penalty CD | 11 months | 4.75% | $0 | None |

CD Basics: What You're Actually Agreeing To

A certificate of deposit is a time deposit — you give the bank your money for a fixed term (typically 3 months to 5 years), and in exchange they give you a guaranteed, fixed APY for the entire term. The guarantee is the key benefit: if rates drop after you open the CD, your rate doesn't move.

The cost: if you need the money before the term ends, you'll pay an early withdrawal penalty — typically 90 to 365 days of interest depending on the bank and term length. On a $10,000 CD, a 270-day penalty at 5.30% is roughly $393.

Who Should Open a CD?

CDs make sense when:

- You have a known future expense (wedding, down payment, tuition) in 6–24 months

- You want to lock in current rates before they fall

- You have cash above your emergency fund that isn't going into investments

- You want a completely guaranteed, predictable return

CDs don't make sense when:

- The money might be needed before the term ends

- You're building your emergency fund (use a HYSA for liquidity)

- You have high-interest debt — pay that off first

CD Strategy: Should You Ladder?

A CD ladder spreads your money across multiple terms to balance rate-locking with flexibility. Example with $20,000:

- $5,000 in a 6-month CD at 5.15%

- $5,000 in a 12-month CD at 5.30%

- $5,000 in an 18-month CD at 5.00%

- $5,000 in a 24-month CD at 4.80%

As each CD matures, you either spend it (if needed) or roll it into a new CD at whatever the current top rate is. You're never more than 6 months away from a liquidity event, but you're capturing higher rates than a savings account on the majority of the money.

The No-Penalty CD Option

Ally's 11-month no-penalty CD at 4.75% deserves a callout. You get a rate close to their standard HYSA, but it's locked — meaning if rates drop, you keep your 4.75%. And if you need the money, you can withdraw anytime after 6 days with no penalty. It's the best of both worlds for cash you probably won't need but want to protect from rate drops.

CD vs. High-Yield Savings Account: Which Wins in 2026?

If current CD rates are 5.30% and HYSA rates are 5.10%, the gap is small. The decision comes down to one question: do you think savings rates will rise or fall from here?

- If rates fall: The CD wins. You locked in 5.30% while the HYSA dropped to 4.00%.

- If rates rise: The HYSA wins. Your CD is stuck at 5.30% while HYSAs move to 6.00%.

- If rates stay flat: The CD slightly wins on rate, HYSA wins on flexibility.

The Federal Reserve's direction matters here. Most economists as of May 2026 expect gradual rate cuts over the next 12–18 months, which would push HYSA rates down while CD rates stay locked. That environment favors locking in a CD now.

For a deeper comparison, see our article on HYSA vs Money Market vs CD.

Best CD Picks by Use Case

Best for Locking In the Highest Rate: Marcus 12-Month CD

At 5.30% with a $500 minimum, Marcus's 12-month CD is the best pure rate available from a major FDIC-insured bank. The 270-day early withdrawal penalty is steep, so only open this with money you're confident you won't need.

Best No-Minimum CD: Ally Bank

Ally requires no minimum deposit on their CDs, making them accessible for people just starting to build savings. Their no-penalty CD at 4.75% is particularly compelling for anyone with uncertainty about their timeline.

Best Short-Term CD: SoFi 6-Month

If you have a known expense in 6 months (a tax bill, a vacation, a planned purchase), SoFi's 6-month CD at 5.15% locks in a great rate with only a 90-day early withdrawal penalty as downside protection.

Frequently Asked Questions

Are CDs safe?

Yes. CDs from FDIC-insured banks are protected up to $250,000 per depositor per bank. Credit union CDs are covered by NCUA insurance at the same limit. Your principal is as safe as any bank deposit.

What happens when a CD matures?

At maturity, most banks give you a grace period (typically 7–10 days) to withdraw the money or roll it into a new CD. If you do nothing, the CD usually auto-renews at the current rate for the same term — which may be higher or lower than your original rate. Set a calendar reminder for your maturity date.

Can I open multiple CDs at the same bank?

Yes. Each CD is a separate account, so you can have a 6-month CD and a 12-month CD at the same bank simultaneously. This is the basis of the CD ladder strategy described above.

Is the interest on CDs taxable?

Yes. Interest earned on CDs is taxable as ordinary income in the year it's credited to your account (even if you don't withdraw it until maturity on a multi-year CD). The bank will send you a 1099-INT form each year.

Budget Blueprint Kit

Zero-to-surplus budgeting done in an afternoon. PDF guide, auto-calculating Excel tracker, and AI prompt library included.

$27 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.