Three accounts, all paying 4–5%+ in 2026, all FDIC insured, all better than your old savings account. The difference is in the details — and those details matter a lot depending on whether you might need the money next month, have a known expense in 12 months, or want maximum flexibility with no lock-in.

Here's the complete breakdown so you can match the right account to your actual situation.

Free Resource

Want a complete wealth-building roadmap?

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →Side-by-Side Comparison

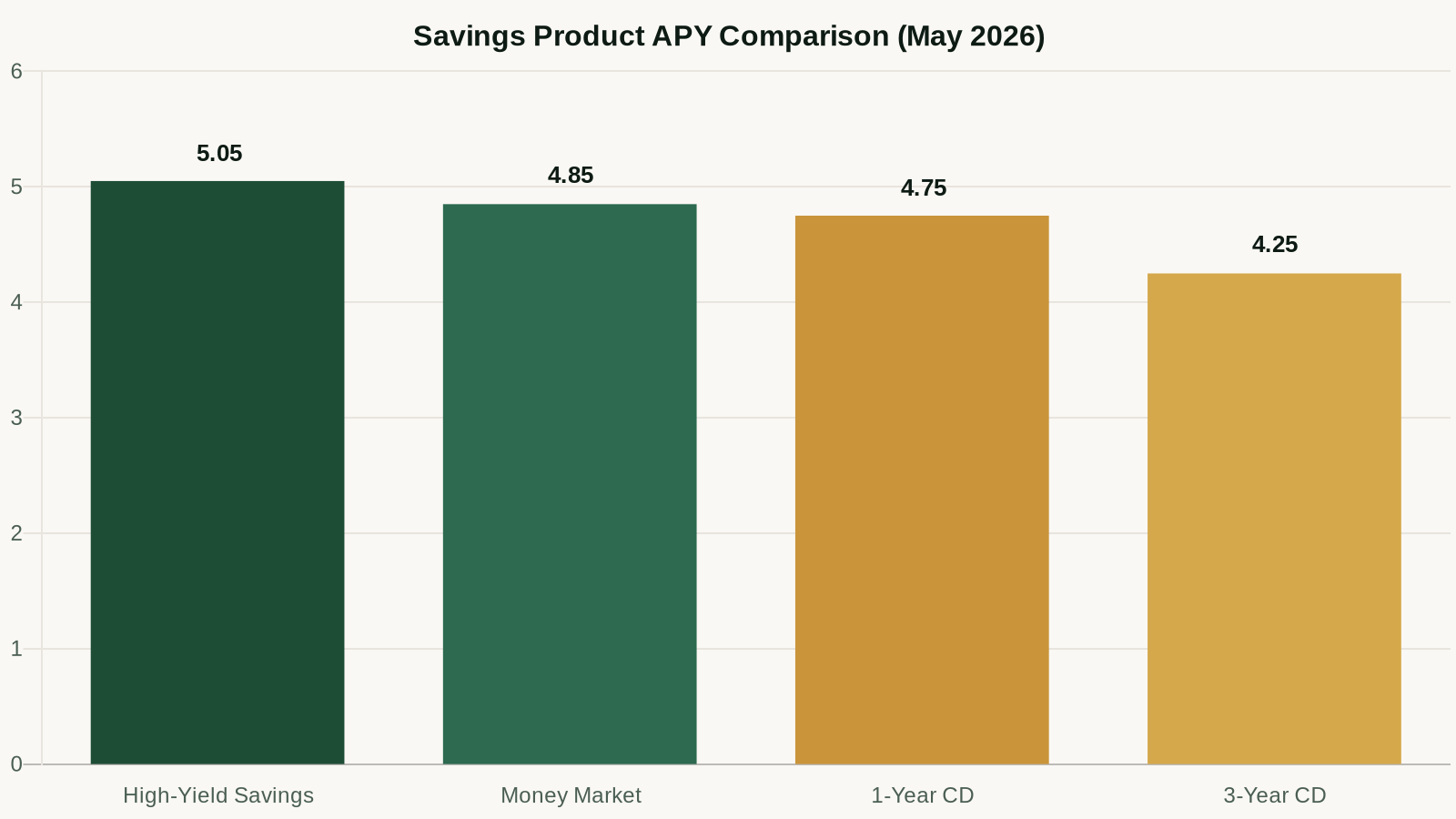

| Feature | HYSA | Money Market Account | CD |

|---|---|---|---|

| Typical APY (May 2026) | 4.75–5.10% | 4.50–5.00% | 4.80–5.30% |

| Rate type | Variable (can change) | Variable (can change) | Fixed (locked for term) |

| Liquidity | High (withdraw anytime) | High (withdraw anytime) | Low (penalty for early exit) |

| Best for | Emergency fund, short-term savings | Large cash balances, check-writing | Known future expense, rate lock-in |

| Minimum deposit | Usually $0 | Often $1,000–$10,000 | Usually $500–$2,500 |

| Check-writing? | No | Sometimes | No |

| FDIC insured? | Yes | Yes | Yes |

High-Yield Savings Accounts (HYSA): The Flexible Default

A HYSA is the simplest, most flexible option. You deposit money, earn a variable rate, and can withdraw it whenever you need it (transfers typically take 1–3 business days). Rates move with Federal Reserve policy, so when rates rise, HYSAs benefit — and when rates fall, HYSAs drop.

Best for:

- Your emergency fund — needs to be accessible without penalty

- Short-term savings with an uncertain timeline

- Anyone who values simplicity and doesn't want to think about it

- People building savings who don't yet have enough for a CD minimum

Top HYSA picks:

- SoFi — 5.10% APY, $0 minimum, $0 fees

- Marcus — 4.90% APY, $0 minimum, Goldman Sachs backing

- Ally — 4.75% APY, full banking ecosystem

Money Market Accounts (MMA): The Middle Ground

A money market account is a hybrid between a savings and checking account. You earn interest (competitive with HYSAs), but you also get check-writing privileges and sometimes a debit card. The tradeoff: higher minimum balances and sometimes higher monthly fees.

Money market accounts are NOT the same as money market funds. A money market account at a bank is FDIC insured. A money market fund is an investment product — slightly higher risk, not FDIC insured.

Best for:

- People with larger cash balances ($10,000+) who want occasional check-writing

- Business accounts that need to pay vendors directly from savings

- People who want a slight rate premium over HYSAs at some institutions

When an MMA doesn't make sense:

- If you don't need check-writing, a HYSA is simpler and often pays the same or more

- If you can't meet the minimum balance without fees, the fee erodes your interest

Certificates of Deposit (CD): Lock In Your Rate

A CD gives you a fixed, guaranteed rate for a specific term — typically 3 months to 5 years. The rate doesn't move, even if the Fed cuts rates next month. You agree upfront that you won't touch the money until maturity (or pay a penalty if you do).

Best for:

- A known future expense: wedding, down payment, tax bill in 12 months

- Locking in today's rates if you believe rates will fall (likely in 2026)

- The portion of your savings above your emergency fund that you're confident you won't need

CD risks to know:

- Early withdrawal penalties are real — don't open a CD with money you might need

- If rates rise significantly, you're locked into a lower rate

- Inflation can erode real returns on longer-term CDs at current rates

See our full Best CD Rates of 2026 guide for specific picks and ladder strategies.

Which Account Should You Choose? (Decision Framework)

Answer these questions in order:

- Is this your emergency fund? → HYSA. Liquidity is non-negotiable for emergency money.

- Might you need this money in the next 6 months? → HYSA or no-penalty CD.

- Do you have a specific expense in 6–24 months? → CD. Lock in the rate and match the term to your timeline.

- Do you have $50,000+ and want occasional check-writing? → Consider an MMA.

- Everything else? → HYSA is the default. Simplest, most flexible, most liquid.

The Case for Using All Three

A sophisticated savings structure uses all three tools:

- HYSA: 3–6 months emergency fund + any savings with uncertain timeline

- CD ladder: Savings earmarked for known future goals (6, 12, 18, 24-month CDs)

- MMA: Only if you have a specific need for check-writing on a larger cash balance

Most people don't need an MMA. A HYSA for liquidity and CDs for time-bound goals covers the majority of scenarios.

Frequently Asked Questions

Are money market accounts safe?

Yes, if they're bank money market accounts (not money market funds). Bank MMAs are FDIC insured up to $250,000 per account category. Credit union MMAs are covered by NCUA at the same limit. Always confirm the account is bank-based and FDIC insured before depositing.

Can I have all three accounts at the same time?

Absolutely. Many people keep their HYSA at Ally or SoFi, open CDs at Marcus for the best rates, and skip the MMA entirely. There's no rule against holding multiple savings products simultaneously — in fact, it's the recommended approach for larger savings balances.

Which account is best if interest rates fall?

CDs win when rates fall — you've locked in today's higher rate for the full term. HYSAs and MMAs will drop along with the Fed. If you expect a rate cut cycle (which most economists project for late 2026), it's worth locking in CDs now on the portion of savings you won't need for 12–24 months.

Is there a limit on how much I can keep in a HYSA?

No limit to what you deposit, but FDIC coverage is capped at $250,000 per depositor per bank. If you have more than $250,000 in cash savings (rare for most people), spread it across multiple FDIC-insured institutions. SoFi offers up to $2M in FDIC coverage through partner banks, which covers most situations.

Budget Blueprint Kit

Zero-to-surplus budgeting done in an afternoon. PDF guide, auto-calculating Excel tracker, and AI prompt library included.

$27 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.