Your credit score is one of the most powerful numbers in your financial life. It determines whether you qualify for a mortgage, what interest rate you pay on a car loan, and in some cases whether you land your dream job. Yet millions of Americans are flying blind — unaware of errors dragging their scores down or threats quietly eroding their financial identity.

The good news: a new generation of credit monitoring and repair tools makes it easier than ever to take control. Whether you need real-time alerts, dispute help, or a full credit overhaul, there is a service built for your situation.

Credit Monitoring vs. Credit Repair: What's the Difference?

Before diving in, it helps to understand what each type of service actually does:

- Credit Monitoring tracks your credit reports in real time and alerts you to changes — new accounts opened in your name, score fluctuations, suspicious activity, or hard inquiries. Think of it as a security system for your financial identity.

- Credit Repair involves actively disputing inaccurate, outdated, or unverifiable negative items on your credit reports. A reputable service sends dispute letters to the three major bureaus (Equifax, Experian, and TransUnion) on your behalf and may also negotiate with creditors.

Most people benefit from both — monitoring to stay aware, and repair services if negative items are weighing down your score.

Free Resource

Want a clear roadmap for your finances?

Get the free Wealth Assimilation Starter Kit — covers income, saving, and investing basics in one downloadable guide.

Download Free Starter Kit →Our Top Picks at a Glance

| Service | Best For | Starting Price |

|---|---|---|

| SmartCredit ⭐ #1 Overall | All-in-one monitoring + active score building | $19.95/mo |

| Credit Karma | Free monitoring (no cost) | Free |

| Lexington Law | Professional attorney-backed credit repair | $89.95/mo |

| myFICO | True FICO score monitoring for loan prep | $19.95/mo |

| Credit Saint | Best money-back guarantee | $79.99/mo |

| IdentityIQ | Identity theft + credit monitoring bundle | $29.99/mo |

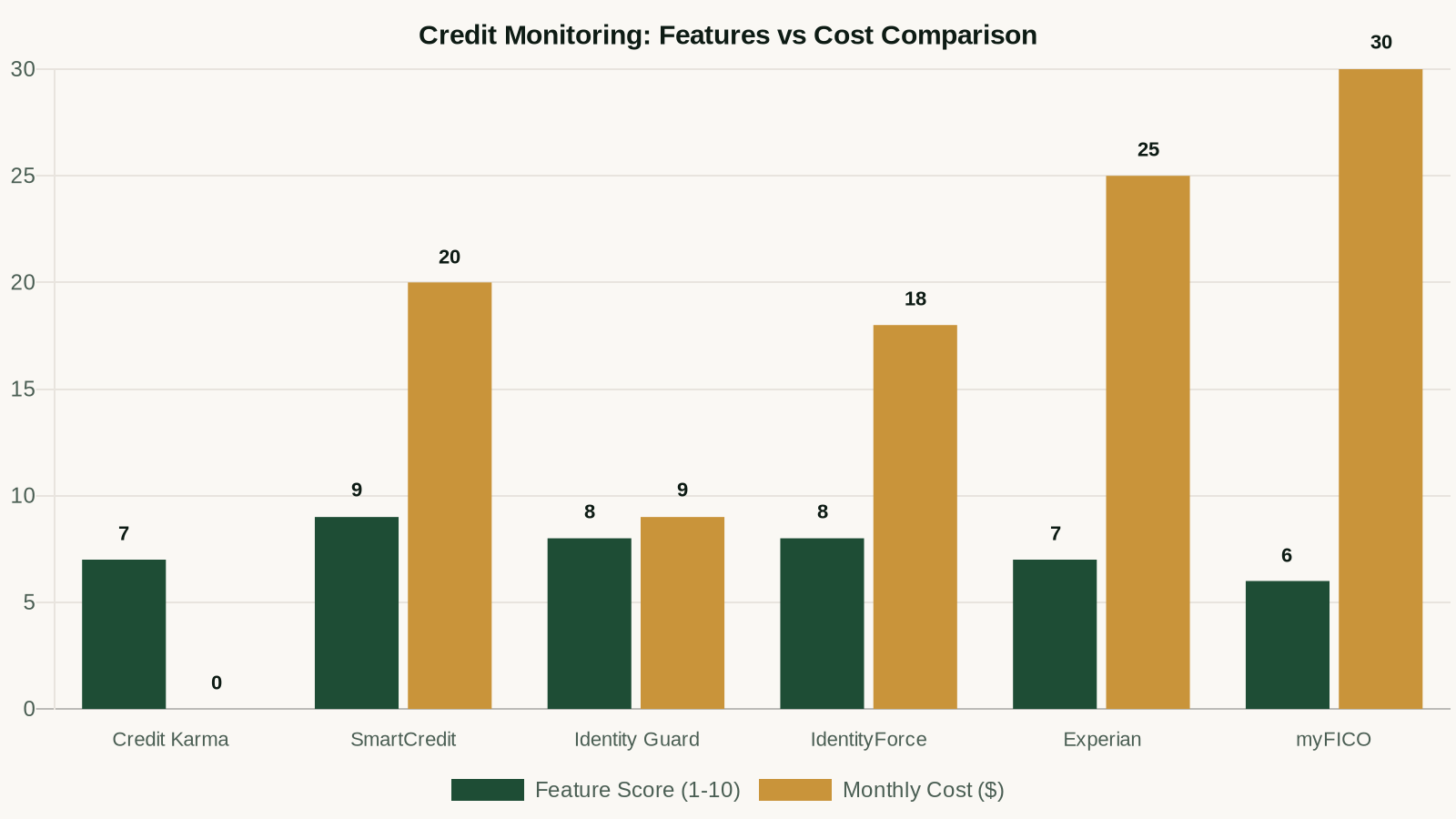

#1 Best Overall: SmartCredit

If you are serious about not just watching your credit — but actively improving it — SmartCredit is our top recommendation for 2026. SmartCredit has been empowering consumers since 2003, built by ConsumerDirect, a fintech company dedicated to giving everyday Americans the insights and tools they need to navigate their financial futures.

Unlike passive monitoring apps that simply show you numbers, SmartCredit gives you an interactive platform that tells you what to do next — and by how much each action will move your score.

What Makes SmartCredit Stand Out

- ScoreBoost™ shows you exactly which accounts to pay down and by how much, with projected score impact in real points — before you take any action. The timing feature ensures your payment registers before your creditor reports to the bureaus, maximizing utilization impact.

- ScoreBuilder® generates a personalized 120-day credit action plan tailored to your unique credit situation — not a generic checklist, but a step-by-step roadmap built around your specific derogatory items, utilization rate, and credit mix.

- Three-Bureau Monitoring gives you full visibility across Equifax, Experian, and TransUnion, all in one dashboard.

- PrivacyMaster® continuously scans data broker websites and databases for your personal information and initiates removal requests — a feature that costs $10–$15/month standalone elsewhere.

- $1 Million Family Identity Fraud Insurance with no deductible, covering all household members.

The average SmartCredit user following their ScoreBuilder plan sees a 61-point credit score increase within just over a month of consistent use. Plans start at $19.95/month with a 7-day free trial.

For a full breakdown of every feature, pricing tier, and real user results, read our complete SmartCredit review.

Best Free Option: Credit Karma

For anyone who wants credit visibility without spending a dime, Credit Karma remains the gold standard for free monitoring. With over 130 million members, it is the most widely used free credit platform in the U.S.

Credit Karma provides free access to your TransUnion and Equifax credit scores (using the VantageScore 3.0 model), weekly score updates, and personalized recommendations for credit cards and loans matched to your credit profile.

What You Get for Free

- Weekly credit score updates (TransUnion & Equifax)

- Credit report monitoring with change alerts

- Personalized financial product recommendations

- Free tax filing and savings account tools

- Identity monitoring alerts

The trade-off: Credit Karma's model is ad-supported. You won't get Experian monitoring or true FICO scores. For deeper score management and active improvement tools, pair it with SmartCredit.

Check Your Free Credit Score on Credit Karma →

Best for Active Credit Repair: Lexington Law

When DIY dispute letters aren't getting results, Lexington Law brings in the attorneys. Founded in 2004, Lexington Law has helped over 500,000 clients repair their credit and has facilitated the removal of over 70 million inaccurate negative items from credit reports.

Plans range from $89.95 to $129.95/month — higher priced, but justified when you need aggressive, legally-backed credit repair for complex negative items that haven't responded to standard dispute letters.

Best for FICO Score Accuracy: myFICO

Here is something most people don't realize: the score Credit Karma shows you is a VantageScore — not the FICO score that 90% of top U.S. lenders actually use when making credit decisions. If you are preparing for a mortgage or major loan, you need to know your actual FICO score.

myFICO is the consumer division of FICO, the company that invented the scoring model. It provides genuine FICO scores across all three bureaus, plus the mortgage-specific, auto-specific, and credit card-specific score versions lenders actually pull. Plans start at $19.95/month.

Best Money-Back Guarantee: Credit Saint

Credit Saint's 90-day money-back guarantee removes the risk from trying credit repair. If they can't remove any negative items from your credit history within the first 90 days, you get a full refund — one of the most consumer-friendly policies in the industry. Three plan tiers: Credit Polish ($79.99/mo), Credit Remodel ($109.99/mo), and Clean Slate ($139.99/mo).

Best for Identity Theft Protection: IdentityIQ

IdentityIQ bridges the gap between credit monitoring and full identity theft protection. For people worried about data breaches, dark web exposure, or fraud, IdentityIQ delivers comprehensive coverage including three-bureau monitoring, dark web scanning, court records monitoring, and up to $1 million in identity theft insurance. Entry plans start at $6.99/month; full coverage runs $19.99–$29.99/month.

How to Choose the Right Service

| Your Situation | Best Choice |

|---|---|

| Good credit, want to protect and grow it | SmartCredit + Credit Karma (free) |

| Significant negative items or errors on report | Lexington Law + SmartCredit for monitoring |

| Preparing for a mortgage or major loan | myFICO (see your lender score) + SmartCredit (optimize it) |

| Experienced identity theft or data breach | IdentityIQ (most comprehensive protection) |

| Want to start without spending money | Credit Karma (free baseline) |

Building Credit from Scratch

If you're starting from zero, monitoring won't help much until you have accounts to monitor. Read our guide on how to raise your credit score fast for the step-by-step process. Once you have established accounts, SmartCredit's ScoreBuilder plan becomes your most powerful tool for systematic improvement.

Understanding what is a good credit score and what factors drive it is also essential context before choosing a monitoring or repair service. If your score issues are tied to high credit card utilization, consider a balance transfer card as part of your paydown strategy.

The Bottom Line

Your credit score is not just a number — it is a financial multiplier that affects the cost of everything from your mortgage to your car insurance. The services on this list represent the best tools available in 2026 to help you monitor, protect, and build your credit.

Our top recommendation remains SmartCredit because it is the only platform that combines real-time three-bureau monitoring with actionable score improvement tools. Users routinely report 50–100 point score improvements within months of following their personalized plan. The 7-day free trial makes it risk-free to see what your specific credit file needs.

Or if you want the full picture before deciding, our in-depth SmartCredit review covers every feature, real user results, and a complete pros and cons breakdown.

Frequently Asked Questions

Is credit monitoring worth paying for?

It depends on your goals. If you only need basic score visibility, Credit Karma is free and sufficient. If you're actively trying to improve your score, dealing with negative items, or preparing for a major loan, a paid service like SmartCredit ($19.95/mo) delivers tools that directly move your score — making the subscription self-funding through better loan rates and terms.

Will credit monitoring hurt my credit score?

No. Credit monitoring services use soft pulls to check your credit, which do not affect your score at all. Only hard inquiries from actual credit applications impact your score.

How long does credit repair take?

It depends on what's on your report. Simple errors can be corrected in 30–45 days (one billing cycle for bureaus to update). Legitimate negative items — late payments, collections, charge-offs — take longer and are harder to remove. Services like SmartCredit's ScoreBuilder help you prioritize the actions with the highest score impact first, compressing your timeline.

What's the difference between VantageScore and FICO?

VantageScore is the model used by Credit Karma and most free services. FICO is the model used by approximately 90% of U.S. lenders for credit decisions. Both use a 300–850 scale and similar factors, but they weight factors differently — so your VantageScore and FICO score may differ by 20–50 points. If you're applying for a mortgage, check myFICO for your actual lender-facing score.

The AI Money Machine

Turn AI into a full-time revenue engine. Monetize AI tools across content, consulting, and digital products — zero prior experience needed.

$47 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.