Albert Einstein (probably didn't actually) call compound interest the eighth wonder of the world — but whoever said it was right. Compound interest is why $100/month invested at 25 is worth dramatically more than $300/month invested at 45. It's also why carrying a $5,000 credit card balance at 24% APR can cost you more than the original purchase in interest over time. Understanding how it works changes how you think about every financial decision you make.

What Is Compound Interest?

Simple interest: you earn interest on your original principal only. If you deposit $1,000 at 5% simple interest, you earn $50/year, every year.

Compound interest: you earn interest on your principal AND on the interest you've already earned. That $1,000 at 5% compounded annually:

- Year 1: $1,000 × 5% = $50 interest. Balance: $1,050

- Year 2: $1,050 × 5% = $52.50 interest. Balance: $1,102.50

- Year 3: $1,102.50 × 5% = $55.13 interest. Balance: $1,157.63

- Year 10: Balance: $1,628.89

- Year 30: Balance: $4,321.94

Same $1,000. No additional contributions. Just 30 years of compounding. The original $1,000 became $4,322 with zero additional effort.

The Numbers That Should Change Your Behavior

| Monthly Investment | Start Age | End Age | Total Contributed | Final Value (7%) |

|---|---|---|---|---|

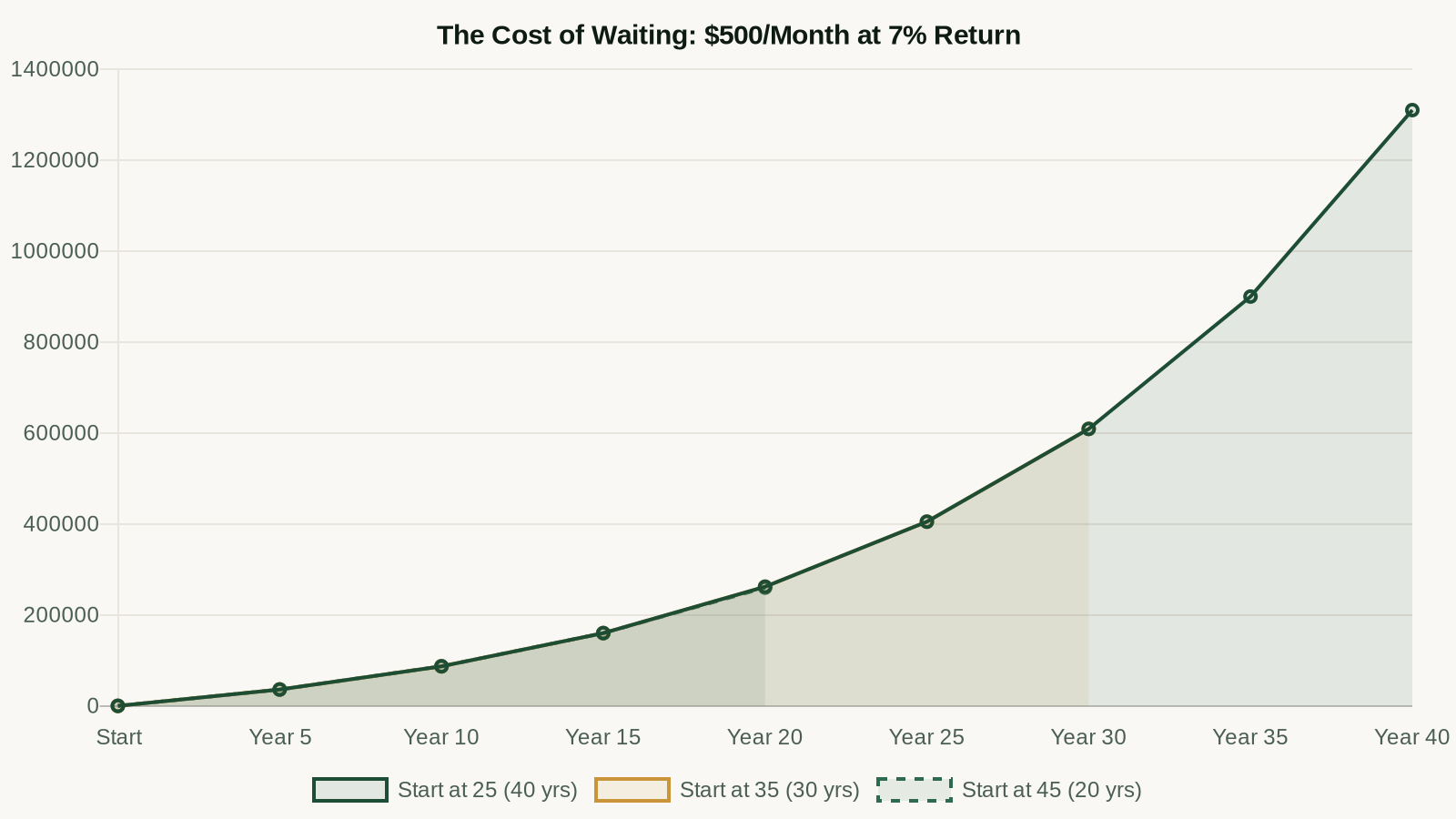

| $500/month | 25 | 65 | $240,000 | $1,310,000 |

| $500/month | 35 | 65 | $180,000 | $609,000 |

| $500/month | 45 | 65 | $120,000 | $260,000 |

| $1,000/month | 35 | 65 | $360,000 | $1,218,000 |

Notice the comparison between the first and second row: starting at 25 with $500/month produces $1,310,000. Starting at 35 with $500/month produces $609,000 — even though you contributed only $60,000 less total. The 10-year head start is worth $701,000. That's the cost of waiting.

Also notice the last row: if you wait until 35 and double your contribution to $1,000/month (contributing $360,000 total vs. $240,000), you still end up with less ($1,218,000 vs. $1,310,000) than if you had started earlier with half the monthly contribution. More money cannot fully compensate for starting later.

Compounding Frequency: Does It Matter?

Interest can compound at different frequencies: annually, quarterly, monthly, or daily. More frequent compounding means slightly higher effective returns:

- $10,000 at 5% compounded annually for 10 years: $16,289

- $10,000 at 5% compounded monthly for 10 years: $16,470

- $10,000 at 5% compounded daily for 10 years: $16,487

The difference is small at these rate levels. What matters far more is the rate itself and the time horizon. Monthly compounding (common in HYSAs and investment accounts) is effectively the same as daily for practical purposes.

The Rule of 72: Mental Math for Compounding

The Rule of 72 is a quick way to estimate how long it takes money to double: divide 72 by the interest rate.

- 5% return → 72 ÷ 5 = 14.4 years to double

- 7% return → 72 ÷ 7 = 10.3 years to double

- 10% return → 72 ÷ 10 = 7.2 years to double

- 24% credit card APR → 72 ÷ 24 = 3 years for your debt to double

That last number is the horror story. A $5,000 credit card balance at 24% APR doubles to $10,000 in just 3 years if you're making minimum payments. Compound interest doesn't care whether it's working for you or against you.

Compound Interest Working Against You: Debt

Every form of debt with compound interest is compounding working in the wrong direction. The same force that turns $500/month into $1.3M over 40 years also turns a $5,000 credit card balance into a decade-long financial anchor.

This is why eliminating high-interest debt before investing (beyond the employer match) is mathematically correct: there is no guaranteed investment return that beats a guaranteed 20–24% debt elimination. See our guide on how to pay off debt fast for the avalanche and snowball methods.

How to Maximize Compound Interest Working for You

1. Start Earlier (The Highest-Leverage Action)

The tables above make the case clearly. If you haven't started investing yet, today is better than tomorrow. Don't wait until you have "enough" — $50/month invested for 40 years at 7% is $131,000. Start now.

2. Increase Your Rate of Return

Every percentage point of return compounds over decades. Moving from 5% to 7% by investing in stock index funds instead of keeping cash in savings adds hundreds of thousands of dollars over a working lifetime. The risk tolerance required to achieve this — staying invested through market downturns — is the price of admission.

Open a Fidelity Account — Zero-Fee Index Funds →

3. Minimize Fees and Taxes

Fees and taxes reduce your effective return, which slows compounding. A 1% expense ratio on a fund costs you ~25% of your ending wealth over 30 years. Using zero-cost index funds and tax-advantaged accounts (Roth IRA, 401k) eliminates most of this drag.

4. Reinvest Dividends

Index funds and stocks pay dividends. Reinvesting those dividends — rather than taking them as cash — adds to your compounding base. Most brokerage accounts have automatic dividend reinvestment (DRIP) that you can enable for free.

5. Never Interrupt the Compounding

Selling investments to time the market, withdrawing from retirement accounts early, or pausing contributions during a downturn all interrupt compounding at precisely the wrong moments. The biggest compounding killer is behavior — specifically, selling during fear and missing the recovery.

If you want compound interest to work automatically — with tax-advantaged accounts, automatic rebalancing, and no fund-picking required — Betterment is designed exactly for this. Set your target, contribute monthly, and let compounding do the rest.

Start Compounding with Betterment →

Frequently Asked Questions

Does compound interest apply to savings accounts?

Yes. High-yield savings accounts compound interest monthly or daily. At 5.10% APY, $10,000 compounds to $10,510 in year 1, $11,047 in year 2, and $16,600 in year 10 — without adding a single dollar. The compounding is less dramatic than investments because the base rate is lower, but it's still meaningfully better than simple interest.

What's the difference between APR and APY?

APR (Annual Percentage Rate) doesn't account for compounding. APY (Annual Percentage Yield) does. When comparing savings accounts or loans, use APY for an apples-to-apples comparison. A savings account that compounds monthly at 5% APR has an APY of approximately 5.12%.

How does compound interest work in a 401(k)?

A 401(k) doesn't pay interest in the traditional sense — it holds investments (stocks, bonds, funds) that grow in value and pay dividends. When dividends are reinvested and the portfolio grows, you're benefiting from compounding in the same mathematical sense. The 7% historical average used in most retirement calculations reflects this compounded growth over time.

Can I lose money to compound interest?

Compounding works on debt exactly as it does on investments. Credit card debt at 24% APR compounds monthly — meaning unpaid interest gets added to your principal, and next month's interest is calculated on the higher balance. This is how minimum payments keep people in debt for years: most of the payment goes to interest, not principal, so the balance barely moves.

10 Income Streams Blueprint

Build 10 distinct income streams with AI doing the heavy lifting. 42-page system, 30-day plan, done-for-you tracker.

$97 one-time

Keep Reading

Get the Free Wealth Starter Kit

The step-by-step guide to your first $100K. Account setup, investment priorities, and a 12-month action plan.